Cargo liability explained: Avoid costly risks for trucking fleets

- Guyorguy Laguerre

- May 6

- 11 min read

TL;DR:

Cargo theft losses increased 60% in 2025, reaching $725 million across 2,646 incidents, with an average of $274,000 per event. Understanding cargo liability as a standalone legal obligation and implementing proper documentation, GPS tracking, and security measures can significantly reduce claim denials and financial risks. Building a strong cargo liability culture and reviewing policies regularly helps fleets protect against theft, loss, and denial, ensuring better claims outcomes and lower insurance costs.

Cargo theft losses surged 60% to $725 million in 2025, with 2,646 incidents recorded and an average loss of $274,000 per event. That is not a statistic buried in a niche trade report. That is money walking off your trucks, out of your accounts, and into a legal dispute you may not even win. Most fleet owners assume their general commercial policy covers everything that moves on their trailers. Many find out the hard way, often mid-lawsuit, that cargo liability is a distinct area of law and insurance with its own rules, triggers, and traps. This guide breaks it all down so you can make smarter decisions before a loss happens, not after.

Table of Contents

Key Takeaways

Point | Details |

Strict liability reality | Under federal law, carriers are almost always responsible for cargo loss unless a rare exception applies. |

Avoidable claim denials | Over 80 percent of denied claims are due to preventable documentation errors. |

Rising financial risks | Cargo theft and loss are escalating, averaging $274,000 per incident in 2025. |

Process is protection | Following strict claim and documentation workflows shields your business from major losses. |

Tech reduces premiums | Using GPS tracking and modern security typically lowers insurance premiums by 5 to 10 percent. |

What is cargo liability? Legal foundations and core concepts

Cargo liability refers to the financial and legal responsibility a carrier holds for the goods it agrees to transport. If freight is lost, stolen, damaged, or delivered in worse condition than it was received, the carrier is the first party held accountable. This applies whether you operate five trucks or five hundred.

It is a common misconception that cargo liability is just a subset of general commercial property insurance. It is not. Your property policy covers your physical assets, your buildings, your equipment. Your auto insurance covers accidents on the road. Cargo liability is a standalone obligation that attaches the moment your driver signs the bill of lading and accepts those goods for transport. Understanding the difference between these liability coverage types is one of the first things every fleet operator needs to get right.

The legal backbone for most cargo liability disputes in interstate trucking is the Carmack Amendment. Under 49 U.S.C. §14706, carriers are presumed liable for loss or damage to freight from the moment they accept it to the moment it is delivered. That word “presumed” is the key. You do not need to prove the carrier was negligent. The shipper simply shows the freight was in good condition when loaded and in worse condition when delivered, or that it never arrived at all.

“The Carmack Amendment essentially places the burden of proof on the carrier. Unless you can prove one of five specific defenses, you are liable.” This shifts the default position in ways that surprise many fleet operators who assume fault must first be demonstrated.

The five defenses that can break that presumption are narrow and hard to prove:

Act of God: An extraordinary natural event beyond human control, such as a tornado directly striking the truck.

Act of the shipper: The shipper’s own improper packaging, labeling, or loading caused the damage.

Inherent vice: The goods deteriorated due to their own natural properties, not because of anything the carrier did.

Act of public enemy: Damage caused by a declared enemy of the state, which in practice is rarely applicable.

Act of public authority: A government agency legally seized or destroyed the goods.

Notice that weather delays, road accidents, and cargo theft by unknown third parties generally do NOT qualify as valid defenses on their own. That is why learning the full scope of your motor carrier insurance basics is so important before you sign the next contract.

How cargo claims work: The process and pitfalls

Knowing when you are liable matters, but it is equally vital to understand how claims get paid or denied. The gap between a successful claim and a rejected one often comes down to what happened in the first 60 minutes after a loss event, not the policy limits.

Here is how a typical cargo claim unfolds:

Discovery: The driver, receiver, or dispatcher identifies that goods are missing, damaged, or short-shipped. This is the moment the clock starts ticking.

Evidence collection: Photos, driver notes, seal logs, and temperature records (if applicable) are gathered at the scene and at delivery. This is your foundation.

Filing the claim: A formal written claim is submitted to the carrier’s claims department with supporting documentation. Most policies require filing within nine months of the delivery date or the expected delivery date.

Investigation: The carrier’s insurance company reviews the bill of lading, proof of delivery, driver logs, photos, and any police reports to assess what happened and who is at fault.

Resolution: The claim is paid, partially paid, or denied. Denials trigger either negotiation, dispute, or litigation.

The process looks clean on paper. In practice, it is full of ways things can go wrong for your fleet. Claims frequently fail due to poor documentation, late reporting, missing photos, and BOL exceptions that were never recorded at the time of delivery. A driver who accepts a damaged shipment without noting the damage on the bill of lading has essentially handed the shipper a clean slate to blame the carrier entirely.

Here is a real-world scenario that illustrates the contrast. Two trucks from the same fleet each deliver electronics on the same Tuesday morning. Truck A arrives and the receiver notices one pallet has water damage. The driver photographs the damage, notes the exception on the bill of lading before signing, and calls dispatch immediately. The claim is filed that afternoon with photos, signed BOL, and a temperature log. It pays out in full. Truck B has a similar situation, but the driver is in a hurry, signs the clean POD without noting damage, and calls dispatch three days later. The claim is filed two weeks after delivery. It is denied because the carrier cannot prove the damage happened in transit rather than after delivery.

Same day. Same fleet. Completely different outcomes.

Scenario | Documentation | Filing Timeline | Outcome |

Truck A | Photos, BOL exception, temp log | Same day | Claim paid in full |

Truck B | Clean POD signed, no photos | 14 days after delivery | Claim denied |

Theft with GPS data | GPS record, police report, seal log | Within 48 hours | Partial to full payment |

Theft with no records | No GPS, no police report | 3 weeks later | Denied |

Pro Tip: Train every driver to treat every delivery exception as a potential claim. The 10 minutes it takes to photograph damage and note it on the BOL can mean the difference between a $200,000 payout and a $200,000 loss.

For more practical guidance on strengthening your process, explore these cargo claim insurance tips that fleet managers regularly overlook.

The top risks in cargo liability: Theft, loss, and denial

Having seen how claims play out, the next step is grasping what risks your insurance really needs to protect against. Not all cargo losses are created equal, and the threats facing modern fleets have become more sophisticated than a bolt cutter on a padlock.

The core risks fall into three categories:

Cargo theft: Includes opportunistic theft at truck stops, rest areas, and drop lots, as well as organized cargo theft rings that target specific high-value freight lanes.

Accidental loss or damage: Improper loading, road accidents, weather exposure, temperature failures, and contamination.

Denied claims: This is the hidden risk most fleets fail to account for. A loss you cannot successfully claim is functionally identical to having no coverage at all.

The numbers make the theft risk impossible to dismiss. Cargo theft in 2025 reached 2,646 incidents with total losses of $725 million, a 60% surge from the prior year. At an average of $274,000 per incident, a single theft event can wipe out months of operating profit for a small to midsize fleet.

“The most dangerous cargo theft operations today are not smash-and-grab events. They are coordinated, intelligence-driven operations using fraudulent broker identities, inside information, and digital tracking countermeasures.”

Organized theft rings are a growing threat that deserve specific attention. These groups will often impersonate freight brokers, place fake pickup orders, and disappear with full truckloads before anyone realizes the fraud. Inside jobs, where dispatchers or drivers share route information with external actors, are also increasing. Cyber methods including GPS spoofing, electronic seal bypasses, and phishing of fleet management systems are no longer rare.

For fleets that are uninsured or underinsured against cargo liability, the financial implications go well beyond the immediate dollar loss. You face shipper chargebacks, contract penalties, legal fees, and in serious cases, the loss of carrier contracts with major shippers who require verified cargo coverage minimums. If a shipper drops your fleet after a loss, the resulting revenue gap can be permanent. Looking at strategies to reduce insurance costs while maintaining adequate coverage is a balance every fleet manager needs to actively manage.

The denial risk deserves its own category because many fleet operators do not think of it as a separate risk at all. But a policy that exists on paper and fails at the claims stage is not protecting your business. It is creating false confidence.

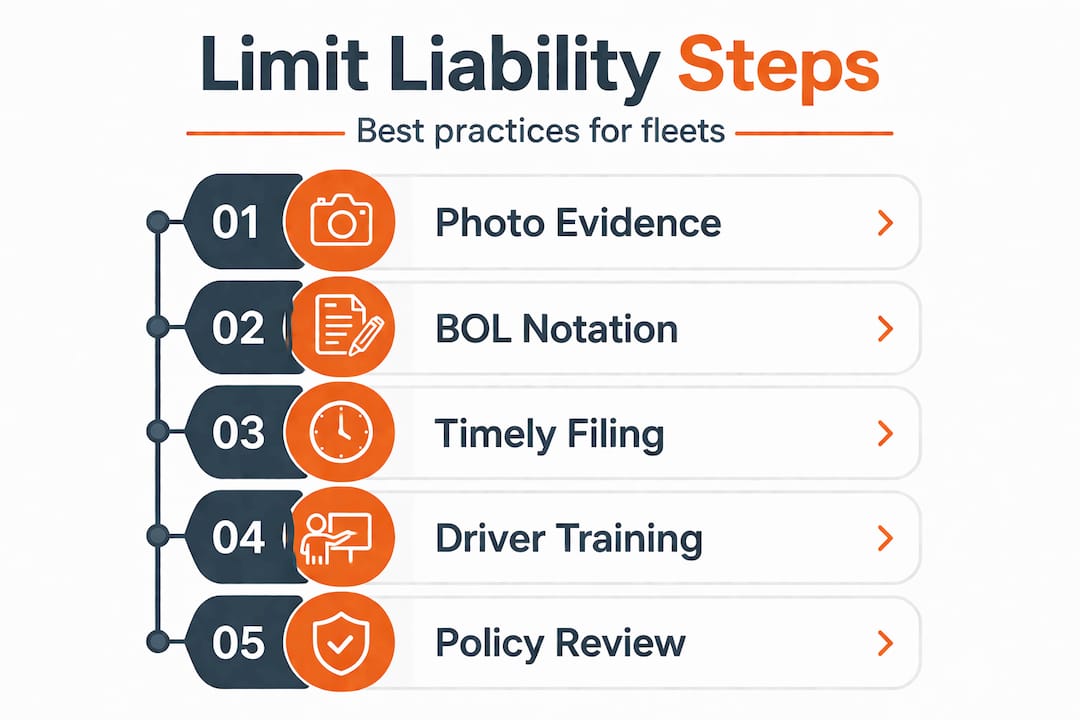

Proven ways to minimize cargo liability exposure

To turn the risks of loss and denial into manageable issues, fleets need to adopt specific, evidence-backed tactics. This is not about adding bureaucracy. It is about building repeatable habits that hold up under scrutiny when a $274,000 claim is on the line.

Here are the foundational steps every fleet should implement:

Establish a documentation workflow: Every driver needs a standardized checklist for pickup and delivery. This includes verifying seal numbers, photographing cargo condition at load, noting any existing damage on the BOL, and confirming receiver signatures on POD documents.

Train drivers on exception notation: A clean BOL is not always a good thing. If a driver signs a clean bill of lading without noting visible damage, your claim window is essentially closed. Regular training reinforces the habit of noting exceptions every single time.

Install GPS and cargo tracking hardware: Real-time GPS provides a verifiable record of a truck’s movements, stop durations, and geofence breaches. This data is often decisive in theft claims.

Use digital proof-of-delivery tools: Paper PODs get lost, smudged, or disputed. Digital timestamped PODs with geo-tagged signatures create an audit trail that is far harder to challenge.

Conduct regular documentation audits: Review a sample of completed BOLs and PODs monthly. Look for patterns, drivers who consistently skip exception notation, routes with recurring discrepancies, and receivers who regularly sign for damaged freight without noting it.

Secure cargo at every stop: Locks, landing gear locks, kingpin locks, and trailer alarm systems are basic but effective deterrents. Avoid parking at unsecured locations overnight whenever possible.

The difference between standard practice and best practice in documentation is measurable. Strict documentation protocols including photos, BOL and POD notes, temperature logs, and seal logs prevent more than 80% of claim denials, and GPS and security investments can reduce premiums by 5 to 10 percent.

Practice area | Standard approach | Best practice | Impact on claims |

BOL notation | Signed as-is | Exception noted with photo | Claim approval rate increases sharply |

Delivery photos | Occasional | Every delivery, timestamped | Disputes drop significantly |

GPS tracking | Basic unit | Real-time with geofencing | Theft claims resolved faster |

Temperature monitoring | None or manual | Automated digital logs | Reefer claims validated easily |

Annual claims review | Reactive | Scheduled audit with patterns | Denial rate decreases year over year |

Understanding how technology adoption affects your premiums is explored in depth when you look at lowering premiums with tech. It is worth reviewing your current setup against what insurers actually reward with discounts.

Fleets that operate leased owner-operators or use vehicles during non-trucking periods should also examine their non-trucking liability coverage to ensure there are no coverage gaps when a unit is technically off-dispatch but still on the road.

Pro Tip: Pull your last 12 months of denied or partially paid claims and categorize every denial reason. If documentation errors appear in more than two claims, you have a process problem, not a bad luck problem. Fix the process, and your claim success rate will improve immediately.

For a broader view of how to structure your risk management approach, reviewing comprehensive fleet risk strategies gives you a framework that connects cargo liability to the full picture of fleet protection.

Why cargo liability mistakes undermine even smart fleets

Here is the uncomfortable truth that most cargo liability guides will not tell you directly: the fleets that suffer the biggest losses are rarely the ones that do not know the rules. They are the ones that know the rules, believe their team is following them, and never actually verify that they are.

There is a significant gap between organizational knowledge and daily execution. A fleet manager can attend every industry webinar, read every compliance guide, and brief every driver on documentation protocols. But if there is no consistent feedback loop, no audit process, no real consequence for skipping a BOL exception, the knowledge stays in the meeting room and never reaches the delivery dock.

The real cost of a cargo loss is also far larger than the claim value. Consider what actually happens after a major loss. The truck is out of service while the investigation runs. The shipper is calling your operations team every day for updates. Your dispatcher is buried in paperwork instead of managing active loads. Your most experienced driver is rattled and working at half capacity. Customer relationships take hits that do not show up on a balance sheet but absolutely affect contract renewals. Morale across the fleet drops when a major incident goes badly.

Experienced fleet leaders understand that cargo liability is not a compliance checkbox. It is a cultural standard. The fleets that consistently win on claims are the ones where drivers take pride in clean documentation, where exceptions are seen as professional thoroughness rather than inconvenience, and where leadership reviews claim data as a performance indicator alongside fuel costs and on-time delivery rates.

Building that culture requires specific actions from leadership. Schedule quarterly documentation reviews. Share anonymized claim outcome data with your team so drivers understand the real-world stakes of their paperwork habits. Recognize and reward drivers who consistently follow documentation protocols. Make the standard visible and consequential.

There is also a real role for external expertise here. Working with insurance brokers who specialize in trucking can close process gaps that even well-run fleets miss. A good trucking insurance specialist reviews your claim history, identifies exposure patterns, and recommends coverage structures that match your actual operational risk, not just a generic carrier profile. They can also identify whether your current policy language actually responds to the scenarios your drivers face every day, something many fleet managers have never formally verified.

The fleets that win are not the ones with the most expensive policies. They are the ones with the clearest processes, the most consistent execution, and the most honest relationship with their own risk profile.

Protect your fleet with the right cargo liability coverage

Understanding cargo liability is only half the equation. Making sure your current coverage actually matches the risks your fleet faces every day is where the work gets real.

Insuaria is built to help trucking businesses take that next step with less friction. Through simple intake forms, Insuaria helps fleet operators and logistics managers organize the details that licensed insurance professionals need to review their coverage situation. Whether you are concerned about gaps in your cargo liability protection or want to ensure your documentation practices align with what your policy actually requires, starting with organized information makes every subsequent conversation more productive. Submit your fleet details through the business insurance intake process to get started, or if you need to review your commercial auto and trucking coverage structure, the truck insurance intake form connects your information directly with licensed professionals who specialize in fleet operations. Insuaria does not bind coverage or issue quotes. Licensed agency partners handle all coverage decisions and recommendations after reviewing your intake submission.

Frequently asked questions

What are the five defenses under the Carmack Amendment?

Carriers can avoid liability by proving an act of God, act of shipper, inherent vice, act of public enemy, or act of public authority. Each defense is narrow and requires clear evidence.

How much has cargo theft increased recently?

Cargo theft surged 60% in 2025, with total U.S. losses reaching $725 million across 2,646 recorded incidents. The average loss per event was approximately $274,000.

What is the number one reason cargo claims are denied?

Poor documentation is the leading cause, specifically missing photos, unsigned BOL exceptions, and late reporting. Clean delivery documentation at the time of the incident is the single most effective way to protect your claim.

Can better tech actually lower my insurance cost?

Yes. GPS and security systems can reduce premiums by 5 to 10 percent for many fleets while also improving claim resolution speed and success rates.

Recommended

Comments