Fleet insurance explained: protect, comply, and lower risks

- Guyorguy Laguerre

- May 1

- 10 min read

Most fleet operators discover the real complexity of trucking insurance at the worst possible moment: after a major claim gets denied, a broker rejects their load because their liability limit is too low, or an audit reveals a coverage gap that’s been sitting there for months. Federal minimums are just the starting point. What lies beneath them, including mandatory endorsements, nuclear verdict exposure, and cargo-specific requirements, is where the real risk lives. This guide cuts through the complexity and gives you a clear, actionable picture of what your fleet actually needs in 2026.

Table of Contents

Key Takeaways

Point | Details |

Fleet insurance simplifies management | Insuring multiple trucks under one policy reduces admin tasks and potential coverage gaps. |

Compliance is not enough | FMCSA minimums often fall short—shippers and brokers usually demand higher coverage and cargo protection. |

Premiums reflect more than your record | Rising 2026 rates are driven by large legal claims, not just individual fleet performance. |

Endorsements close costly gaps | Cargo, increased liability, and specialized coverage are essential for full protection. |

Proactive reviews save money | Regular policy updates and safety investments are the best defense against costly surprises. |

What is fleet insurance and why does it matter?

Fleet insurance is a single insurance policy that covers multiple commercial vehicles under one umbrella. For heavy-duty trucking, that typically means two or more trucks, though most carriers begin to see real administrative and financial benefits at five or more units. As FreightWaves explains, fleet insurance covers multiple heavy-duty trucks under a single policy, simplifying administration, renewals, and often reducing costs compared to individual policies.

This matters more than many operators initially realize. When you’re managing separate policies for each unit, you’re also managing separate renewal dates, separate coverage reviews, and separate premium payments. One missed renewal or a vehicle added late to the wrong policy can create a gap in coverage that a claims adjuster will find immediately when you need them least.

Beyond administration, coverage for trucking fleets under a consolidated policy better aligns your protection with the way your business actually operates. Loads don’t stop at the borders of individual policies. Drivers sometimes operate multiple trucks. And shippers don’t care which vehicle you used when they’re asking for a certificate of insurance.

The core benefits of fleet insurance for heavy-duty trucking operations include:

Single renewal date for all vehicles, reducing administrative burden

Unified claims handling through one insurer and one point of contact

Better premium leverage because insurers offer volume-based discounts

Easier compliance documentation for FMCSA filings and shipper requirements

Blanket coverage for newly acquired vehicles within a policy period (subject to timely notification)

“Fleet operators who manage risk proactively, not reactively, consistently see lower loss ratios, better renewal terms, and fewer surprises when it counts most.”

The risks of inadequate or fragmented coverage go well beyond inconvenience. FMCSA compliance violations can result in out-of-service orders, fines, and even operational shutdowns. One uninsured incident on a $2 million load can end a small carrier’s business before the legal fees even start.

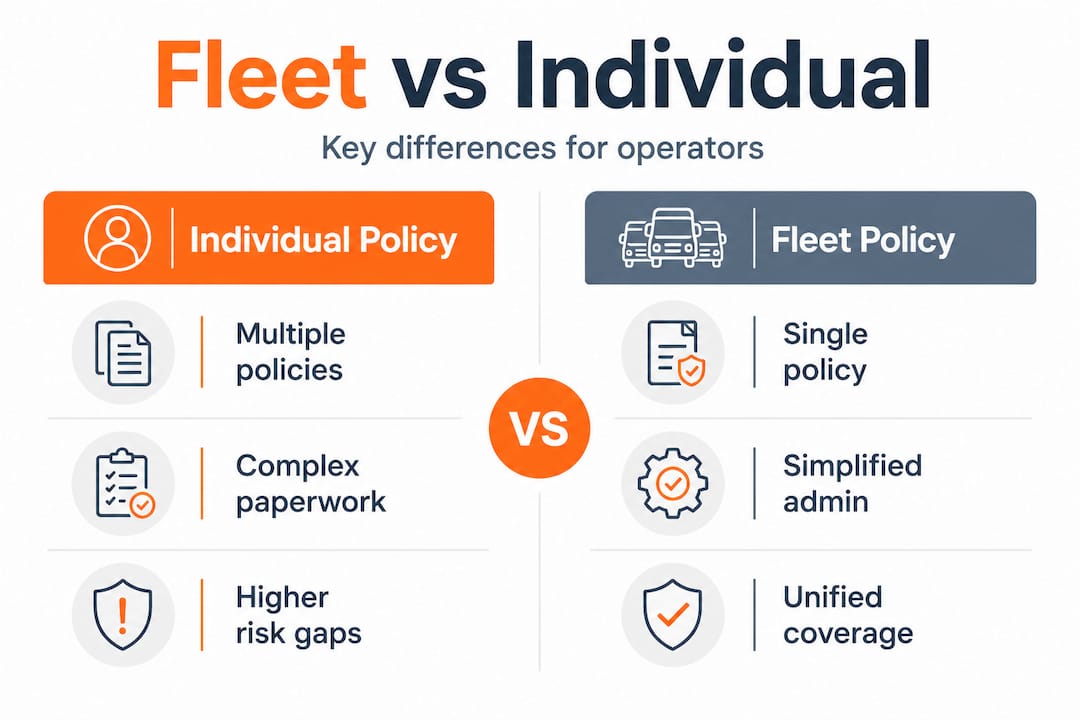

Fleet insurance vs. individual truck policies: The smart comparison

The difference between insuring trucks individually versus under a fleet policy isn’t just administrative. It can affect your cash flow, your cargo coverage, and your ability to win contracts.

Here’s a direct comparison to put it in perspective:

Factor | Individual policies | Fleet policy |

Number of policies | One per truck | Single policy |

Renewal dates | Multiple, staggered | One unified date |

Premium cost (5 trucks) | Higher total cost | Often 15-25% less |

New vehicle addition | Requires new policy | Added by endorsement |

Coverage consistency | Varies by policy | Uniform across fleet |

Administrative time | High | Significantly reduced |

Claims coordination | Multiple adjusters | One point of contact |

A concrete example: A carrier running five owner-operated trucks on individual policies might spend 8 to 10 hours per year managing renewals, certificates, and documentation per vehicle. That’s up to 50 hours annually just on paperwork. A fleet policy can cut that by roughly 30%, freeing your operations team for work that actually moves freight.

Individual policies also create a specific and dangerous risk: coverage gaps when vehicles or drivers change. If a new truck is added to your operation but the individual policy isn’t updated immediately, that vehicle may operate uninsured for days or weeks. Cargo on that truck is also exposed during that window.

Pro Tip: When switching to a fleet policy, audit every vehicle’s current coverage dates and claim history first. Insurers will underwrite based on your fleet’s combined loss record, so you want to know what’s in that record before your broker presents it.

The strategies to reduce fleet insurance costs almost always start with consolidation. Getting all vehicles under one policy gives you negotiating power, a cleaner risk profile, and a foundation for all the optimization work that follows.

Understanding mandatory coverage: FMCSA regulations and real-world requirements

The FMCSA (Federal Motor Carrier Safety Administration) sets the legal floor for liability insurance on interstate commercial vehicles. For heavy-duty carriers operating trucks over 10,001 lbs GVWR, the minimums are clearly defined: $750,000 for general freight, $1 million for oil transport, and $5 million for hazardous materials.

Here’s where many new fleet operators make a costly mistake: they hit the federal minimum and assume they’re done. They’re not.

Cargo type | FMCSA minimum liability | Typical broker/shipper requirement |

General freight | $750,000 | $1,000,000+ |

Oil transport | $1,000,000 | $1,000,000+ |

Hazardous materials | $5,000,000 | $5,000,000+ |

Refrigerated/perishable | $750,000 | $1,000,000 + cargo |

High-value loads | $750,000 | $2,000,000+ |

The practical reality is that most freight brokers and major shippers require at least $1 million in liability coverage, regardless of what FMCSA demands. Some contracts, especially those with retailers or manufacturers handling high-value freight, require $2 million or more. If your liability thresholds for fleets don’t meet what the broker requires, you don’t get the load. It’s that simple.

There are a few key compliance points worth addressing directly:

FMCSA Form BMC-91 or BMC-91X must be filed by your insurer to confirm liability coverage. Without this filing, your operating authority is at risk.

Cargo insurance is not included in your base liability policy. This is a separate endorsement and a separate line of coverage. New fleet operators frequently discover this only after a cargo claim is denied.

Your state may have additional requirements on top of FMCSA minimums, particularly for intrastate operations.

For a complete picture of what motor carrier insurance looks like in practice, including all required filings and endorsements, it’s worth reviewing the full breakdown of what regulators, brokers, and shippers actually expect from your operation.

Key compliance checklist for heavy-duty fleets:

Minimum $750K liability on file with FMCSA (BMC-91/91X)

Separate cargo coverage endorsed on your policy

MCS-90 endorsement on your commercial auto policy (required by federal law)

Physical damage coverage meeting lender requirements if trucks are financed

Workers’ compensation in states where required for employed drivers

Fleet insurance costs in 2026: What’s driving rates?

Let’s talk numbers. Premium rates in 2026 are up significantly, and the reasons behind that increase should change how you think about your coverage strategy.

Annual premiums for general freight carriers with clean records break down roughly like this: owner-operators pay $8,000 to $14,000 per year; small fleets of two to five trucks run $15,000 to $40,000; medium fleets of six to twenty trucks range from $40,000 to $130,000; and large fleets of 20 or more trucks can expect $120,000 to $400,000 or more annually. Rates are up approximately 18.5% in 2026, largely driven by nuclear verdicts, which are jury awards exceeding $10 million in trucking-related lawsuits.

Nuclear verdicts are not rare anymore. They’ve become a consistent factor in how underwriters price commercial trucking risk across the board. Even a carrier with a clean safety record pays higher premiums today because the industry’s overall claims severity has risen dramatically.

The primary factors driving your individual fleet premium include:

Claims and loss history over the past three to five years

Driver experience and MVR (Motor Vehicle Record) quality across your fleet

Route profile, including long haul, regional, or local urban operation

Cargo type, with higher-value or more hazardous freight costing more to insure

Fleet age and vehicle condition

Safety program quality, including whether you use telematics

“Underwriters in 2026 are scrutinizing driver data harder than ever before. A single driver with multiple violations can raise your entire fleet’s premium.”

The path to reducing trucking insurance premiums isn’t mysterious, but it requires consistent effort. Here’s what works:

Implement a telematics program to monitor speed, braking, and driving behavior in real time. Insurers increasingly offer discounts for data-sharing agreements.

Build a formal driver safety training program and document it. Carriers who train regularly see better MVR profiles over time.

Conduct monthly safety meetings and keep records. This demonstrates a proactive safety culture to underwriters during renewal.

Review your loss runs before renewal and address any patterns. If you’ve had multiple cargo claims, look at loading procedures. If liability claims are frequent, review route selection.

Work with a broker who specializes in trucking, not a generalist. Specialists know which carriers are actively competing for your fleet class and can negotiate more effectively.

Key endorsements and common gaps: Cargo, liability, and beyond

Understanding that cargo is not automatically included in a base fleet auto policy is possibly the single most important thing a fleet operator can take from this article. Federal minimums are floors, not ceilings, and practical coverage needs are almost always higher for both compliance and load access. A cargo endorsement must be added separately, and its limits must match what your freight contracts require.

Beyond cargo, here’s where fleets commonly discover gaps at the worst possible time:

New vehicles added but not immediately reported to the insurer. Most policies have a grace period of 30 days, but that window can close without notice.

Non-owned trailer coverage missing. If your drivers haul trailers they don’t own, those trailers may not be covered under your standard policy without a specific endorsement.

Uninsured or underinsured motorist coverage overlooked. Your driver gets hit by an uninsured passenger vehicle. Without this endorsement, your fleet absorbs the loss.

Physical damage limits set at actual cash value instead of replacement cost, leaving you short when a truck is totaled.

Driver exclusions buried in the policy. Some policies exclude coverage when unlisted drivers operate vehicles. If a substitute driver takes a load, you could be exposed.

Pro Tip: Request a policy review at least 90 days before renewal. This gives you enough time to address gaps, negotiate endorsements, and switch carriers if needed without scrambling under deadline pressure.

For commercial auto insurance for fleets, the base policy is just the foundation. Endorsements are what build real protection around it. And for specific guidance on policy construction and coverage decisions, the insurance for trucking companies resources available to fleet operators can make the difference between a policy that holds up under scrutiny and one that falls apart during a claim.

Our take: Why checklists aren’t enough—what actually protects your fleet

We’ve worked with enough fleet operators to see a pattern that repeats constantly. Carriers focus intensely on hitting the legal minimums, file their BMC-91, add cargo coverage because a broker demanded it, and then treat insurance as a done deal until renewal rolls around again. That approach consistently produces the most painful claim stories.

The real danger isn’t non-compliance. Most carriers clear that bar. The real danger is assumed coverage, which happens when operators believe their policy does something it doesn’t. Assumed cargo coverage. Assumed protection for a leased trailer. Assumed coverage for a new hire who drove a run while waiting to be added to the policy. These are the scenarios that create six-figure out-of-pocket losses.

True fleet protection requires treating your insurance program as a living part of your risk management operation, not an annual transaction. That means quarterly policy reviews, not just annual ones. It means building your safety culture around telematics data, not just logging miles. And it means understanding that insurance and ELD compliance are increasingly linked, because electronic logging data can be subpoenaed in litigation and used to challenge or support your coverage position.

The operators who consistently perform best at renewal, meaning they get better rates and broader coverage, are the ones who view their insurance broker as a strategic partner, not a vendor. They share loss run data proactively. They notify their insurer of fleet changes quickly. They invest in driver training not just because it’s required, but because it actually changes their underwriting profile over time.

Technology is the most underused lever in this space. Telematics doesn’t just help you monitor drivers. It creates a defensible record that protects you in litigation and demonstrates to underwriters that you manage risk actively. In a market where rates are up nearly 20%, that distinction can mean a significant premium difference at renewal.

Protect your fleet: Take the next step with Insuaria

Understanding the layers of fleet insurance is the first step. Putting the right structure in place for your specific operation is where real protection starts.

Insuaria specializes in commercial trucking insurance built specifically for fleet operators and logistics companies. From high-limit liability policies to cargo endorsements and FMCSA compliance support, the platform is designed to match your fleet’s actual risk profile with coverage that holds up under pressure. Whether you’re managing five trucks or fifty, getting the right policy structure matters more in 2026 than it ever has. You can request an insurance review directly through the platform, get a tailored quote based on your fleet size, cargo type, and route profile, and get clarity on exactly where your current coverage may be falling short.

Frequently asked questions

Does fleet insurance cover cargo automatically?

No, most fleet policies require a separate cargo endorsement to protect goods in transit. Never assume cargo is included in your base commercial auto policy.

How much liability insurance do I need for my trucking fleet?

FMCSA mandates a minimum of $750,000 for general freight, but most brokers and shippers require $1 million or more to award contracts. Your actual required limit depends on your cargo type and the freight contracts you want to access.

Why are trucking insurance premiums so high in 2026?

Rates are up 18.5% in 2026 primarily because of nuclear verdicts, which are jury awards exceeding $10 million, and rising overall claims severity across the trucking industry.

Can I switch my individual truck policies to a fleet policy mid-year?

Yes, most insurers allow a consolidation move at renewal or mid-term with adequate notice and a full underwriting review. Your broker can coordinate the timing to avoid any coverage gaps during the transition.

What’s the biggest mistake fleets make with insurance?

Most fleets assume they’re fully protected once they meet the federal minimums, missing critical endorsements like cargo coverage and non-owned trailer protection that are essential for real-world operations.

Recommended

Comments