Understand trucking insurance premiums: lower costs and manage risk

- Guyorguy Laguerre

- Apr 27

- 10 min read

Your fleet’s safety record is improving, your drivers are better trained than ever, and you’ve installed the latest collision avoidance technology. So why is your insurance renewal higher than last year? This is the reality facing most commercial trucking operations today. Insurance premiums are climbing faster than general inflation, driven by litigation costs, rising repair bills, and market forces that no single fleet can control. This guide breaks down exactly what fuels premium increases, which coverage choices matter most, and what concrete steps you can take to stay competitive on costs without sacrificing protection.

Table of Contents

Key Takeaways

Point | Details |

Premiums rising fast | Insurance costs for trucking fleets are rising faster than inflation, regardless of recent safety improvements. |

Coverage choices matter | Selecting the right coverage types and deductibles directly affects what your fleet pays each year. |

Hidden cost drivers exist | Litigation, social inflation, and repair costs impact premiums more than most fleet managers realize. |

Action reduces risk | Proactive safety, data sharing, and managing claims are proven ways to control insurance costs. |

What are insurance premiums and how are they determined?

An insurance premium is the amount your fleet pays, usually annually or monthly, for your coverage to remain active. Think of it as the price of transferring financial risk from your operation to an insurer. For commercial trucking fleets, that risk calculation is far more complex than for a personal auto policy, and the variables involved can swing your annual premium by tens of thousands of dollars.

Underwriters look at dozens of data points when pricing your policy. The most influential factors include:

Fleet size and composition: A fleet of 50 semi-trucks operating across state lines carries dramatically different exposure than a 10-truck local delivery operation. Larger fleets get more scrutiny, but they also have more negotiating leverage.

Claims history: Your loss runs, which are the formal records of past claims, are one of the first things an underwriter examines. A single large liability claim can elevate your rates for three to five years.

Coverage limits: Higher liability limits mean higher premiums. Fleets moving hazardous materials or high-value cargo typically need limits well above federal minimums, which raises base costs significantly.

Vehicle type and age: Older equipment that lacks modern safety features costs more to insure and more to repair after an accident.

Operational regions: Fleets that run frequently through urban corridors, congested metros, or high-litigation states face added surcharges. Certain states carry far higher jury award averages, which insurers price in directly.

Driver profiles: Age, license history, MVR (motor vehicle record) violations, and years of experience all feed into how an underwriter scores your driver pool.

Here is a sample overview of how some of these factors shift annual premiums for a mid-size fleet:

Fleet attribute | Annual premium range (estimated) |

10-truck local/regional fleet, clean record | $80,000 to $130,000 |

10-truck fleet with 2+ liability claims | $160,000 to $240,000 |

30-truck OTR fleet, clean record | $300,000 to $500,000 |

30-truck OTR fleet with hazmat operations | $500,000 to $900,000+ |

These are rough benchmarks, not guarantees. Your actual premium depends on your specific risk profile, the insurer’s appetite for trucking business, and current market conditions.

Industry note: Despite real improvements in fleet safety technology and driver training programs, premiums keep rising because litigation costs and vehicle repair expenses outpace safety gains. This is not a temporary blip. It is a structural market shift.

If you are new to the coverage landscape, reviewing truck insurance basics is a smart first step before negotiating your next renewal.

Types of coverage and their impact on premiums

With the basics outlined, the next step is understanding how your coverage choices directly impact what you pay. Commercial trucking policies are not one-size-fits-all. Each coverage type serves a distinct purpose, and the limits and deductibles you select for each one can dramatically affect your total annual cost.

The core coverage categories for trucking fleets include:

Auto liability: This is the most critical and typically most expensive coverage. It pays for bodily injury and property damage you cause to others. Federal minimums start at $750,000 for general freight and reach $5 million for certain hazardous materials operations. Most shippers and brokers require at least $1 million in limits.

General liability: Often called trucking general liability, this covers incidents that occur off the road, such as injuries at a shipper’s dock or product damage during loading. Many fleets overlook this until a claim forces the issue.

Physical damage: This covers your own equipment, divided into collision (accidents) and comprehensive (theft, weather, fire). It is optional in most states but virtually required if your trucks are financed or leased.

Cargo liability: Pays for loss or damage to freight you are transporting. Limits should match the commodity values you regularly haul.

Umbrella or excess liability: Provides additional coverage above your primary liability limits. Given the size of jury verdicts today, fleets without an umbrella layer face serious financial exposure.

How do deductibles fit into this? A higher deductible means you absorb more of each claim before insurance kicks in. Historically, fleets raised deductibles as a strategy to reduce premiums. It worked in softer markets. Today, deductibles keep rising but premiums continue climbing anyway, because the underlying loss costs are too large for deductible adjustments alone to offset. That said, deductible optimization is still a valid tactic when used carefully.

Here is a comparison illustrating how coverage and deductible choices affect typical annual costs for a 20-truck regional fleet:

Coverage scenario | Deductible | Estimated annual premium |

State minimum liability only | $2,500 | $140,000 |

$1M liability + physical damage | $5,000 | $220,000 |

$1M liability + full coverage + cargo | $10,000 | $310,000 |

$2M liability + umbrella + full coverage | $25,000 | $480,000+ |

Pro Tip: Before raising your deductible to cut premium costs, model your cash flow against your average annual claim frequency. If you experience 4 to 6 claims per year, a $25,000 deductible per occurrence could cost you more out of pocket than the premium savings you gain.

You can explore your specific liability coverage options in detail to align your selections with both regulatory requirements and financial exposure. If you are putting together a full coverage strategy, the insurance guide for trucking companies covers policy structuring from the ground up. For comparison, even personal moving insurance basics follow similar deductible logic, which shows how universal the trade-off between deductibles and premiums truly is across the insurance industry.

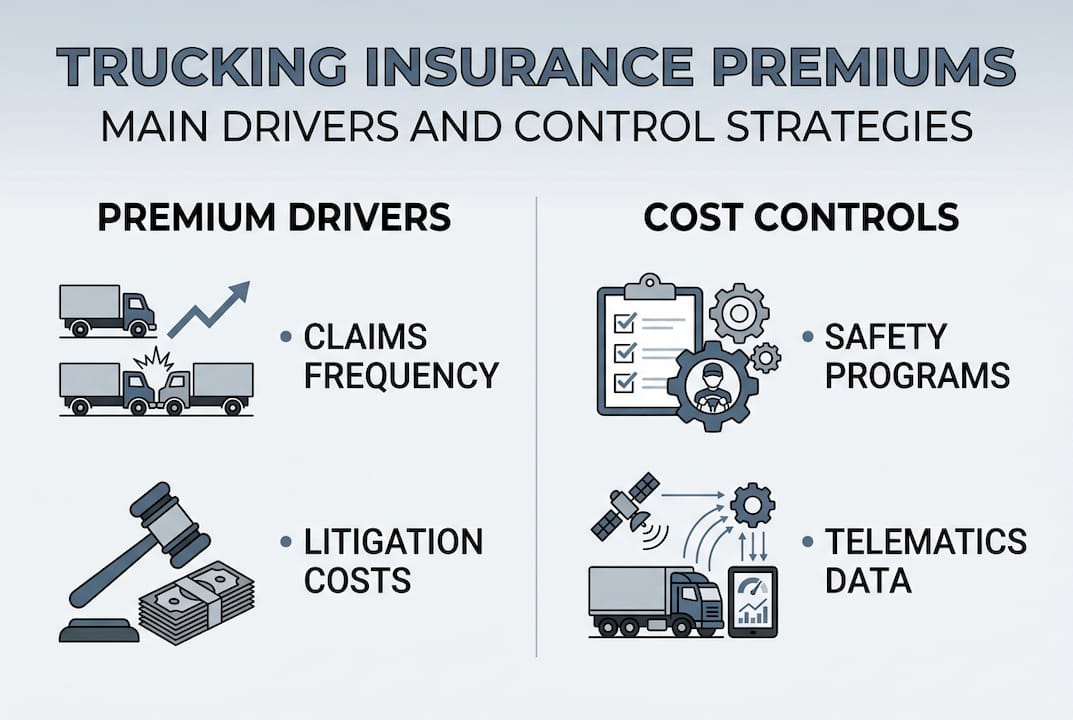

Why are premiums rising? Hidden drivers and risk factors

Armed with coverage understanding, it is crucial to grasp why premiums keep climbing year after year, even when your fleet does everything right. The forces at work here go far beyond your claims history.

“Insurance rates are rising faster than inflation, driven not only by individual fleet behavior but by systemic market forces including litigation funding, nuclear verdicts, and vehicle repair cost inflation.” This represents the emerging consensus forming around rising commercial auto costs.

Here is a numbered breakdown of the real cost drivers:

Litigation funding and nuclear verdicts. Third-party litigation funding, where outside investors finance lawsuits against trucking companies in exchange for a share of the settlement, has dramatically increased the volume and size of trucking lawsuits. Verdicts over $10 million, sometimes called nuclear verdicts, are becoming more common. Insurers price this risk across their entire trucking book, meaning your premium reflects the industry’s legal exposure, not just yours.

Social inflation. This refers to the rising tendency of juries to award large damages in civil cases. It is driven by shifting public attitudes toward large corporations and commercial vehicles. Even a minor accident involving a semi-truck can result in disproportionate jury awards if the case reaches trial. That legal climate raises every fleet’s baseline risk.

Parts and repair cost inflation. Modern trucks are rolling computers. A single collision that would have cost $15,000 to repair a decade ago can now cost $60,000 or more because of sensor arrays, camera systems, and advanced safety modules. Insurers pay those repair bills and price them into renewals.

Medical cost escalation. When truck accidents injure third parties, medical costs are often part of liability claims. Rising healthcare costs feed directly into claim severity, which pushes up premiums across the board.

Reinsurance market tightening. Insurers buy their own insurance, called reinsurance, to manage catastrophic losses. As reinsurers have become more cautious about trucking exposure, primary carriers face higher costs, which get passed on to fleet operators.

Understanding why trucking insurance is expensive at a structural level helps you set realistic expectations and make a stronger case to underwriters. You can also find broader context on logistics risk management strategies that address how supply chain volatility feeds into fleet insurance costs.

Pro Tip: Keep a well-organized documentation package for every renewal. Include safety program records, driver training logs, telematics reports, and any preventive maintenance schedules. Underwriters weight data heavily, and a fleet that presents strong documentation is far easier to underwrite at favorable terms than one that arrives unprepared.

How fleets can manage and control insurance premium costs

Understanding the drivers is only helpful if you can act. Here is how to take charge of premium costs in a market that is working against you.

Active risk management is no longer optional. Despite safety gains and deductible increases, insurance costs persistently rise, which means fleets that wait passively for the market to improve will keep absorbing increases. The fleets seeing the best outcomes are the ones treating risk management as an ongoing operational function, not a once-a-year renewal task.

Immediate actions you can take:

Implement telematics now. GPS and electronic logging data give underwriters hard evidence of driver behavior. Fleets using telematics for fleet management often qualify for credits and can dispute liability in accidents with objective data.

Formalize your driver training program. Documented training, especially defensive driving and hours-of-service compliance, shows underwriters you are serious about loss prevention. Ad hoc training is not enough. You need a written program with completion records.

Review your claims handling process. Slow or poorly managed claims escalate in cost. Partner with your insurer’s claims team early in every incident. A claim reported and resolved quickly costs far less than one that lingers and reaches litigation.

Conduct a thorough driver MVR review. Pull motor vehicle records for every driver annually. High-risk MVR profiles are one of the fastest ways to trigger surcharges. Remove or remediate problem drivers before your renewal.

Long-term strategies for sustained premium control:

Build a safety culture from the top down. Driver buy-in is not automatic. Fleet managers who tie safety metrics to compensation and recognition see measurable improvements in loss frequency.

Diversify your insurer relationships. Relying on a single carrier creates renewal vulnerability. Work with a specialist broker who maintains relationships across multiple trucking-focused markets.

Invest in equipment upgrades strategically. Adding forward-collision warning, automatic emergency braking, and lane-departure systems can qualify your fleet for safety credits on physical damage and liability lines.

Track and analyze your loss ratios over time. Your loss ratio, which is claims paid divided by premiums paid, is a key metric underwriters evaluate. Fleets that monitor and improve this number proactively have more leverage at renewal.

Explore the full range of proven fleet strategies that leading operators use to manage costs without reducing coverage.

Pro Tip: Start your renewal preparation 90 to 120 days before your policy expires. This gives your broker enough time to shop the market thoroughly and gives you leverage to negotiate terms rather than accepting whatever is offered at the last minute.

Our perspective: What most fleets miss about rising insurance premiums

Let us be direct about something the industry does not say loudly enough: shopping for a cheaper quote is not a strategy. It is a reaction. And in today’s market, it is an increasingly ineffective one.

We see fleets put enormous energy into switching carriers every year, chasing a few thousand dollars in savings, while ignoring the underlying cost drivers that will follow them wherever they go. Your claims history, your MVR pool, your documentation quality, those travel with you. A new carrier sees the same risk profile and prices it accordingly.

What actually works is treating insurance as a long-term partnership built on data, communication, and demonstrated commitment to loss control. Fleets that invest in telematics transparency, formalize their safety cultures, and bring organized documentation to every renewal table earn credibility with underwriters. That credibility translates into more competitive terms and more flexibility when a claim does occur.

The fleets winning this battle are not the ones with the lowest premiums today. They are the ones with improving loss ratios year over year, stable carrier relationships, and underwriters who genuinely want to retain their business. That position is built over time, not found by getting better insurance quotes alone.

Insurance is not a commodity for commercial fleets. It is infrastructure. Treat it like one.

Find tailored insurance solutions for your fleet

Rising premiums demand more than a generic policy and a prayer at renewal. Commercial trucking fleets need a coverage partner who understands the difference between a regional flatbed operation and a hazmat carrier, and who can build a policy structure that matches your actual exposure.

At Insuaria, we work exclusively with fleet operators, logistics companies, and trucking businesses that need high-limit, specialized coverage backed by real market expertise. Whether you are navigating your first renewal under today’s difficult conditions or looking to restructure your entire coverage program, our team is ready to help. Start with our fleet insurance inquiry services to connect with a specialist who will review your current program and identify where you have gaps, overpayments, or untapped savings opportunities.

Frequently asked questions

Why do insurance premiums for trucking fleets keep increasing even with safety improvements?

Rates rise faster than inflation because litigation costs, nuclear verdicts, and vehicle repair expenses grow faster than safety improvements can offset, making the overall risk pool more expensive for all fleets.

What fleet actions have the biggest impact on lowering insurance premiums?

Telematics adoption, formal driver safety programs, and proactive claims management deliver the most consistent premium relief, though persistent cost trends mean results take time to show up at renewal.

How do deductibles influence truck insurance premiums?

Higher deductibles reduce your premium, but as industry data shows, premiums are climbing even as fleets raise deductibles, so this approach alone will not stop the upward trend.

What coverage is required by law for trucking companies?

Most trucking operations must carry auto liability and cargo liability at federally mandated minimums, but shipper requirements and state regulations often push the required limits significantly higher than federal floors.

Can shopping for quotes actually lower my insurance premium?

Shopping can surface competitive options, but underwriters evaluate your risk profile regardless of which carrier you approach, making long-term data transparency and loss control more powerful tools than price comparison alone.

Recommended

Comments