Non-trucking liability coverage: What fleet operators need to know

- Guyorguy Laguerre

- Apr 29

- 10 min read

Most fleet operators believe their primary liability policy has them covered no matter what. That assumption is wrong, and it can be expensive. When a leased driver takes a commercial tractor home for the weekend or runs a personal errand between dispatch calls, a coverage gap opens up that most primary policies won’t touch. Non-trucking liability (NTL) insurance is specifically designed to close that gap, but many operators either misidentify it as bobtail coverage or skip it entirely. This article breaks down exactly what NTL covers, how it differs from similar policies, who needs it, and what legal risks come with getting it wrong.

Table of Contents

Key Takeaways

Point | Details |

NTL covers off-duty use | Non-trucking liability fills the gap for personal use of commercial trucks where primary business coverage does not apply. |

Lease requirements matter | Most carriers require NTL by contract, even though it is not mandated by federal law. |

Distinction from bobtail | NTL differs from bobtail insurance by focusing solely on non-business activities, not empty-load travel. |

Legal disputes are common | Coverage disputes often depend on precise contract language and court interpretation. |

Strategic risk management | Treat NTL as a proactive risk tool for fleet protection, not just a compliance checkbox. |

What is non-trucking liability and why does it matter?

Non-trucking liability insurance is a specialized commercial coverage that steps in when a commercial tractor is used outside the scope of business operations. To be precise, as NTL coverage is defined, NTL is designed to cover third-party bodily injury and property damage liability when a commercial tractor is used for personal, non-business activities. Think of it as the off-duty protection layer that keeps your leased operators and your business shielded when work technically isn’t happening.

If you’re new to this coverage type, it helps to understand the commercial truck insurance basics first, because NTL exists within a broader insurance ecosystem, not as a standalone solution. The primary trucking liability policy covers operations conducted under dispatch, meaning when the driver is hauling freight or acting on behalf of the carrier. The moment that dispatch relationship ends, the primary policy typically withdraws its protection. NTL picks up exactly where that policy drops off.

Here’s why this matters in practice. Imagine a leased owner-operator finishes a delivery run on a Friday afternoon. The load is delivered, the paperwork is signed, and the driver heads home in the tractor. Saturday morning, the driver runs a personal errand and gets into an accident. At that moment, neither the motor carrier’s primary liability policy nor the owner-operator’s physical damage policy covers the third-party claim for bodily injury or property damage. Without NTL, that liability falls directly on the operator, and potentially back on the carrier through legal action.

Key situations where NTL provides protection include:

Personal trips made in the tractor between or after dispatched loads

Commuting home from a terminal or drop point in a company-leased unit

Non-commercial errands such as fueling up or maintenance runs initiated by the driver personally

Weekend use when the driver retains the tractor under a lease arrangement but isn’t actively under dispatch

One important distinction: NTL does not replace your primary liability policy. It doesn’t cover accidents that occur while the driver is actively hauling freight, acting under dispatch, or operating in any way tied to the carrier’s business. The two policies operate in clearly defined windows, and both are essential to a complete coverage program.

Motor carriers care about NTL because their primary policy typically has a “business use only” clause. If a leased operator has an off-duty accident and the carrier is named in the lawsuit, the carrier needs to demonstrate it had proper coverage in place for that operator in every operational scenario. Carriers who rely on insurance tips for trucking companies understand that requiring NTL from leased operators isn’t just a formality. It’s a direct line of defense against costly liability exposure.

Stat to keep in mind: The trucking industry accounts for a disproportionately high share of commercial vehicle accident litigation, and off-duty incidents involving commercial tractors are frequently contested in court because the boundary between “personal” and “business” use is rarely obvious without clear documentation and the right policies in place.

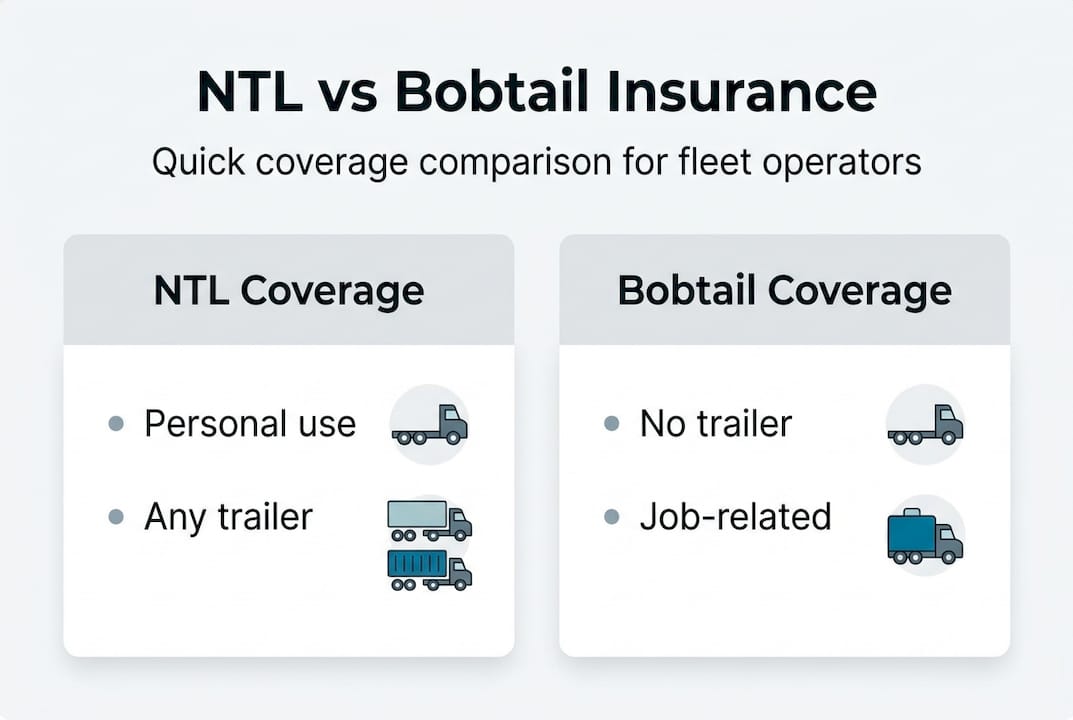

Comparing non-trucking liability and bobtail insurance

This is where most fleet operators and even some brokers get tripped up. NTL and bobtail insurance sound similar, and they serve overlapping protective functions, but they are not interchangeable. Getting this wrong is one of the most common and costly coverage mistakes in trucking.

The cleanest way to understand the difference is this: NTL versus bobtail means that NTL focuses on personal use (off-duty, not business-related) while bobtail focuses on operating without a trailer, often between loads. Bobtail coverage applies any time a tractor is operated without a trailer, regardless of whether the driver is technically on or off duty. NTL applies based on purpose, not on whether a trailer is attached.

Here’s a direct comparison to make this concrete:

Feature | Non-trucking liability (NTL) | Bobtail insurance |

Coverage trigger | Personal, non-business use of tractor | Operating without a trailer attached |

Trailer required? | May or may not have trailer attached | No trailer present |

On-duty coverage? | No, only off-duty personal use | Yes, can apply between loads while on duty |

Typical requirement | Lease agreement with carrier | Carrier policy or owner-operator decision |

Primary policy interaction | Fills gap when primary policy is inactive | Fills gap when primary policy doesn’t apply |

Example scenario | Driver runs personal errands on weekend | Driver returns empty from delivery to pick up next load |

To make this even clearer, consider two drivers. Driver A drops a load in Dallas, unhooks the trailer, and drives the bobtail tractor to a truck stop to wait for the next assignment. Driver A is still under dispatch, operating without a trailer. Bobtail insurance applies here. Driver B finishes a route, drops the trailer at the terminal, and takes the tractor home. On Sunday, Driver B takes the family to a hardware store. NTL applies here, not bobtail.

The confusion often leads fleet operators to purchase one and assume it handles both situations. It doesn’t. A driver without proper NTL could face a six-figure bodily injury claim that falls entirely on their personal assets because the off-duty errand wasn’t covered.

Pro Tip: When reviewing coverage for leased owner-operators, check both what the lease agreement requires and what the driver actually has. A gap between the two is where claims turn into lawsuits. Review your bobtail insurance guide for coverage specifics and regional pricing considerations.

Understanding this distinction isn’t academic. It determines how claims are processed, which insurer responds, and whether your fleet is exposed to co-liability in an off-duty incident.

Who needs non-trucking liability? Lease language, compliance, and risk

Many fleet operators assume that if a coverage isn’t federally mandated, it’s optional. With NTL, that logic is risky. While the FMCSA does not require NTL at the federal level, carriers require NTL for leased owner-operators and leased drivers through the lease agreement itself, even though FMCSA does not federally mandate it.

That distinction matters. It means that a leased operator who doesn’t carry NTL isn’t just unprotected. They may also be in direct violation of their lease, which can trigger penalties, contract termination, and personal financial liability in the event of a claim.

Here’s a practical breakdown of who typically needs NTL and why:

Leased owner-operators who operate under a carrier’s authority and take their tractors home or use them between dispatches

Drivers under permanent lease arrangements where the tractor remains in the operator’s control outside of business hours

Fleet operators who lease equipment to contract drivers and need to verify individual coverage before the driver takes the unit off-lot

Logistics companies contracting with owner-operators who must ensure contractual compliance before allowing any operation under their authority

Lease agreements in trucking are dense documents, but the insurance clauses carry the most legal weight. A typical clause might read something like: “Lessee agrees to maintain non-trucking liability insurance with limits of no less than $1,000,000 per occurrence during any period in which the tractor is not under the Lessor’s dispatch.” That’s a specific requirement with a specific limit, and violating it can void the lease and expose both parties to litigation.

The certificate of insurance (COI) is the documentation that proves compliance. Carriers should require updated COIs from all leased operators at policy renewal and keep them on file. A COI that lists the carrier as an additional insured on the NTL policy provides a critical layer of protection.

Pro Tip: Build a COI renewal calendar for every leased operator in your fleet. NTL policies can lapse quietly, and a lapsed policy on a leased unit creates a direct liability window for the carrier. Cross-reference this with your motor carrier insurance guide to ensure your lease review process aligns with compliance best practices.

For operators navigating regulatory and contractual obligations together, ELD compliance and insurance requirements often intersect in ways that affect policy eligibility and audit readiness. Maintaining clean operational records supports both compliance and favorable insurance terms.

Key legal challenges and coverage disputes in NTL

Compliance gets you in the door, but it doesn’t guarantee a smooth claim. Legal disputes over NTL coverage are more common than many fleet operators realize, and the stakes are high. Understanding how courts handle these disputes can shape how you structure your policies and lease language.

The core issue in most NTL disputes is scope. Was the insured actually performing personal, non-business activities at the time of the incident? Or was there any connection to the carrier’s business that could trigger the primary policy instead? Courts evaluate which policy applies based on whether the insured is acting within the scope that the policy covers, and coverage disputes can hinge on classification and related contractual factors.

“The scope of use at the time of the incident is the central question in almost every NTL dispute. Policy language alone doesn’t decide the case; the facts of what the driver was doing at that exact moment do.” This principle guides courts in determining which insurer bears responsibility.

Common legal scenarios in NTL disputes include:

Dispute type | Trigger | Common outcome |

On-duty vs. off-duty conflict | Driver was “released” from dispatch but remained near terminal | Courts look at dispatch records and timing |

Trailer attachment question | NTL policy excludes trailer use; trailer was present | NTL insurer may deny; bobtail insurer may respond |

Business detour rule | Driver made a personal stop during an otherwise business trip | Primary policy may still apply depending on state law |

Lease ambiguity | Lease doesn’t clearly define “non-business use” | Courts interpret against the drafter (typically the carrier) |

Best practices for avoiding NTL coverage disputes:

Document dispatch release times with timestamps that match ELD records so the “off-duty” window is indisputable

Specify trailer use in lease language so there’s no ambiguity about whether NTL applies when a trailer is attached

Align policy definitions between the primary liability policy and the NTL policy to avoid competing definitions of “business use”

Review all COIs to confirm NTL coverage dates and limits match what the lease requires

Consult with legal counsel before drafting or renewing lease agreements that contain insurance mandates

Understanding the types of liability coverage available in commercial trucking helps fleet managers identify gaps before they become disputes. Additionally, reducing insurance costs without sacrificing coverage quality requires knowing exactly what each policy covers and where exposures remain. For a deeper look at what drives premium levels, the insurance cost factors behind trucking policies explain why NTL pricing varies so widely by fleet type, driver history, and operational territory.

The legal environment around NTL is evolving. Plaintiff attorneys have become skilled at arguing that off-duty incidents still fall within the scope of business use, particularly when the driver was using a carrier-branded tractor or was heading to or from a carrier facility. Having airtight documentation and clearly written policies is your best protection.

The uncomfortable truth most fleets miss about NTL

Most fleets treat NTL as a box to check during lease onboarding. Require it, collect the COI, file it away, and move on. That’s understandable given how many compliance items fleet managers handle daily. But it’s also how coverage gaps quietly accumulate into significant financial exposure.

The real value of NTL isn’t just in having the policy. It’s in actively managing it as part of a broader risk strategy. Policy limits that made sense three years ago may not be adequate today. Lease agreements drafted before recent court decisions may have language that creates unintended ambiguity. And drivers who once had adequate personal coverage may have let policies lapse without notifying your compliance team.

Thinking of NTL as a dynamic risk tool, rather than a static document, changes how you manage it. Annual reviews of the liability coverage guide alongside your NTL requirements can surface outdated language, insufficient limits, or missing carrier requirements before they matter in court. The fleets that treat this coverage as operational infrastructure rather than a paperwork formality are the ones that come through off-duty incidents without lasting financial damage.

Protect your fleet with smarter liability coverage

Non-trucking liability is a precise, essential tool in any serious fleet’s risk management program. Knowing what it covers, how it differs from bobtail insurance, and how courts interpret it puts you ahead of most operators in the industry.

At Insuaria, we work directly with fleet operators and logistics professionals to build liability programs that account for every operational scenario, including the off-duty gaps that most generic policies miss. Whether you’re reviewing lease agreements, managing leased owner-operators, or building a coverage stack from scratch, commercial trucking coverage tailored to your fleet’s real risk profile is what separates adequate from protected. Reach out through our insurance inquiry services to connect with a specialist who can review your current NTL requirements and identify where your fleet stands today.

Frequently asked questions

What does non-trucking liability insurance actually cover?

Non-trucking liability insurance covers bodily injury and property damage when a commercial tractor is used for non-business, personal activities outside the scope of carrier dispatch.

Is NTL required by law for owner-operators?

No, NTL is not federally mandated by the FMCSA, but the majority of carriers require it through lease agreements as a condition of operating under their authority.

How is NTL different from bobtail insurance?

NTL covers off-duty personal use regardless of trailer attachment, while bobtail applies when the tractor is operated without a trailer, which can occur during on-duty periods between loads.

What legal issues can arise with NTL coverage?

Coverage disputes typically hinge on whether the driver was truly off-duty and acting outside business scope at the time of the incident, with courts determining which policy responds based on the facts of the specific situation.

Recommended

Comments