How insurance brokers save trucking fleets time and money

- Guyorguy Laguerre

- Apr 28

- 9 min read

Most trucking companies either overpay for coverage or get turned away by standard carriers altogether, and the gap between those two outcomes often comes down to one factor: whether you have the right broker in your corner. For new trucking authorities, full coverage packages including $1M liability and $100K cargo can run $14,000 to $30,000 per truck annually, with new operations typically paying 40 to 60% more than seasoned fleets. That gap is real money. And a specialized broker can close it faster than most fleet owners realize.

Table of Contents

Key Takeaways

Point | Details |

Brokers expand market access | Insurance brokers connect trucking fleets to specialized and surplus lines insurers, making it easier to secure coverage in tough markets. |

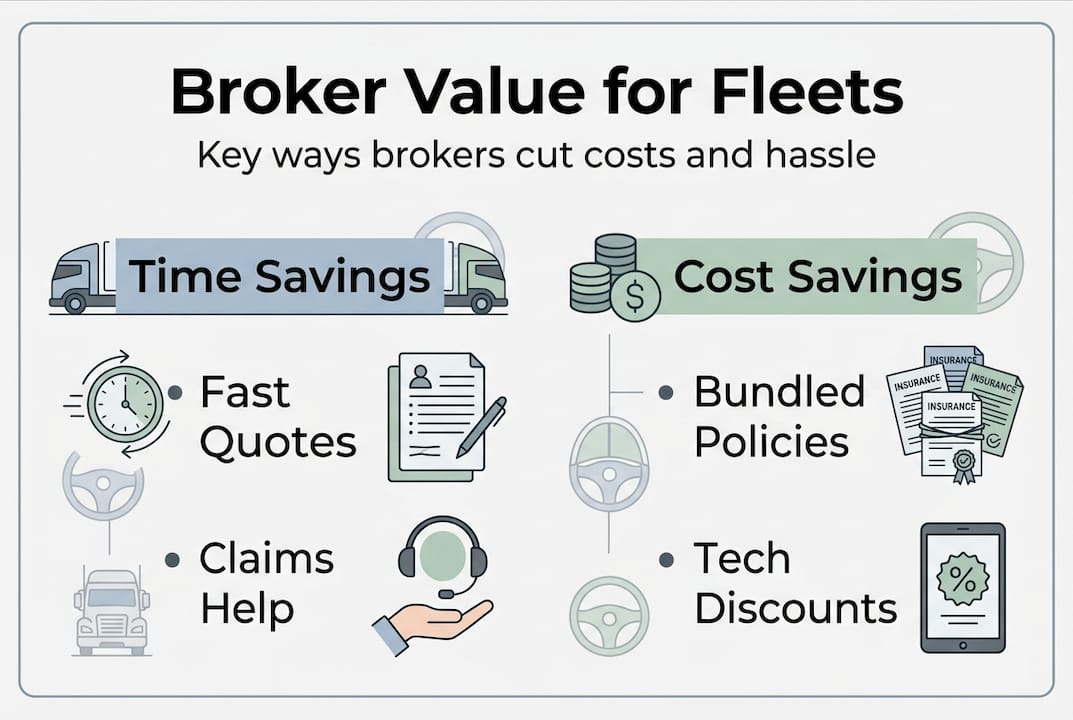

Cost-saving opportunities | Brokers help fleets save 5-25% through bundling and risk technology that direct insurers may not offer. |

Expert risk and compliance support | Professional brokers guide fleets in meeting regulatory requirements and defending against costly claims or premium hikes. |

Advanced solutions for fleet challenges | Modern brokers use captives, higher deductibles, and telematics to address escalating claims costs and litigation risks. |

Why trucking insurance is different and difficult

Commercial trucking insurance operates in a fundamentally different environment than standard business coverage. Rates are more volatile, carrier appetite is narrower, and the regulatory landscape adds a layer of complexity that catches many fleet operators off guard. Understanding why trucking insurance costs are high starts with recognizing the unique risk profile carriers see when they look at your fleet.

Freight tonnage, cargo type, operating radius, driver experience, and prior claims all feed into an underwriting model that is more granular than almost any other commercial line. Add in mandatory federal filings, state-specific requirements, and the ever-rising cost of nuclear verdicts in trucking litigation, and you have a market that penalizes uninformed buyers heavily.

Here are the core factors that make trucking insurance uniquely challenging:

New authority status. Carriers with less than 12 months of operating history are viewed as high-risk by most standard insurers. Many simply decline to write these accounts.

Claims history follow-through. A single serious claim can shadow a fleet for years, with post-claim increases of $2,000 to $5,000 per year for 3 to 5 years, compounding the financial impact well beyond the original incident.

Commodity exposure. Fleets hauling hazardous materials, refrigerated goods, or high-value electronics face surcharges that generalist agents rarely know how to mitigate or negotiate.

Regulatory filings. The FMCSA requires Form MCS-90 endorsements and BMC-91 or BMC-34 filings. Missing a filing deadline can trigger operating authority suspension, which creates cascading insurance and business problems.

Driver turnover risk. High turnover rates in trucking mean underwriters scrutinize driver qualification files, MVR records, and training programs as part of every renewal cycle.

“The trucking insurance market is not just more expensive than other commercial lines. It is structurally harder to navigate because the underwriting variables are more numerous and more consequential.” This is a reality every fleet manager needs to internalize before shopping for coverage on their own.

Standard business owners often treat insurance as a commodity purchase. Fleet managers who take that approach in trucking consistently end up underinsured, overcharged, or both. Reading up on insurance tips for trucking companies before your next renewal cycle can help you walk into those conversations better prepared.

How insurance brokers unlock coverage and savings

Once you understand how difficult the trucking insurance market actually is, the broker’s role shifts from “nice to have” to genuinely essential. The core advantage brokers provide is market access, specifically access to surplus lines carriers and specialty programs that standard agents cannot offer.

When a new trucking authority approaches a direct insurer, the answer is often a flat decline or a quote priced so high it’s barely workable. A broker who specializes in trucking can take that same account to non-admitted surplus lines markets where underwriters are specifically set up to handle high-risk or hard-to-place fleets. The surplus lines market access for new authorities is one of the most practical reasons to work with a broker before you ever haul your first load.

Here is how the direct insurer vs. broker experience typically compares:

Factor | Direct insurer (standard) | Broker-sourced (specialty) |

New authority coverage | Often declined | Available via surplus lines |

Carrier options | One to three | Ten or more |

Premium for new authority | High, limited negotiation | Competitive, structured programs |

Regulatory filing support | Minimal | Comprehensive |

Claims advocacy | Carrier handles only | Broker advocates for fleet |

Bundling options | Limited | Cross-carrier bundling available |

The step-by-step process a skilled broker follows looks like this:

Risk profile analysis. The broker collects your operating data, cargo types, driver records, loss runs, and authority history to build a complete underwriting submission.

Market placement. The submission goes to multiple carriers simultaneously, including specialty and surplus lines markets, to generate competing quotes.

Coverage structuring. The broker reviews each quote for gaps in coverage, not just price, and recommends the program that fits your actual operational risk.

Regulatory filings. The broker handles MCS-90 endorsements and FMCSA filings so your operating authority stays protected.

Ongoing optimization. At renewal, the broker renegotiates with carriers using your updated loss history and any risk improvements you’ve made.

Pro Tip: Ask your broker specifically about bundling your liability, cargo, physical damage, and general liability under a single program. Insurance bundling benefits typically translate to 5 to 15% savings compared to placing each coverage separately with different carriers. That savings on a $25,000 annual premium is real cash back in your operation.

Brokers also help you understand which strategies to reduce trucking insurance costs are realistic for your fleet size and risk profile, rather than applying generic advice that may not work in your specific situation. And when it comes time to shop the market, working with a broker changes the entire dynamic of getting the best trucking insurance quotes because you have professional representation, not just a form submission.

Advanced broker strategies: Technology, risk, and compliance

The best trucking insurance brokers in 2026 are not just market connectors. They are risk engineers who use technology, data, and program structures that most fleet owners have never encountered through a generalist agent.

Telematics integration is the biggest single opportunity most fleets are not fully leveraging. Installing ELD-integrated telematics systems and AI-equipped dashcams gives underwriters hard data on driver behavior: hard braking events, speeding patterns, hours-of-service compliance, and real-time location tracking. Underwriters reward this transparency because it shifts the fleet from “unknown risk” to “documented, managed risk.” The difference in premium impact is substantial: telematics programs can reduce premiums 15 to 25% when the data demonstrates consistent safe driving practices.

Beyond telematics, experienced brokers structure programs using two advanced tools that the standard market does not offer:

Higher deductible programs. By accepting a larger per-incident deductible (often $5,000 to $25,000), fleets can access significantly lower base premiums. This works well for established operators with strong cash reserves and a clean loss history.

Captive insurance programs. In a captive, a group of similar trucking businesses essentially self-insures a portion of their risk through a shared structure. Profits from low-claim years stay within the group rather than flowing to a commercial carrier. This is a sophisticated tool that brokers help fleets evaluate and enter when the conditions are right.

Here is a realistic look at what combined strategies can deliver:

Strategy | Typical premium savings |

Coverage bundling | 5 to 15% |

Telematics/AI dashcam program | 15 to 25% |

Higher deductible structure | 10 to 20% |

Clean loss history improvement | 8 to 18% over 3 years |

Safety training documentation | 3 to 7% |

Understanding how telematics lowers insurance rates in practice is something a broker can walk you through in concrete terms, including which systems carry the most underwriter credibility. Not all telematics providers are treated equally when underwriters review your submission.

Compliance support is another area where broker value is consistently underestimated. A good broker tracks your DOT authority status, ELD compliance requirements, and certificate of insurance expirations. A lapsed filing or a missed certificate request can shut down a load, and in worst cases, trigger a CSA audit. Brokers who specialize in liability insurance options for trucking fleets understand the full compliance picture, not just the policy documents.

Pro Tip: At your next broker meeting, ask specifically what compliance monitoring services are included. A broker who tracks your filings proactively is worth considerably more than one who only shows up at renewal.

Selecting the right broker for your fleet

Not all brokers are equipped to handle commercial trucking accounts at the level your fleet requires. Choosing the wrong one can mean missed markets, poor coverage structuring, and no support when a claim gets complicated.

Here is a practical evaluation checklist:

Trucking specialization. The broker should place the majority of their book in commercial trucking, not treat it as a side segment of a general commercial practice.

Surplus lines access. They should have established relationships with admitted and non-admitted (surplus lines) carriers so new authorities and high-risk accounts have real options.

Technology adoption. The broker should actively recommend and help implement telematics programs, not just ask about them during the application process.

Compliance infrastructure. They should offer ongoing filing support, certificate management, and DOT compliance monitoring as part of their service model.

Claims advocacy track record. Ask for specific examples of how they’ve supported a client through a contested or complex claim.

Top questions to ask before you commit to a broker:

How many trucking fleets of similar size and commodity type do you currently represent?

Which surplus lines markets do you have direct access to, and how many quotes will you generate for my submission?

What happens when I have a claim: do you advocate for me directly, or does the carrier manage everything independently?

How do you handle mid-term changes to my fleet, such as adding trucks, changing lanes, or adding drivers?

Brokers who specialize in the heavy trucking segment understand the full market cycle in ways generalists simply cannot. As one industry-level analysis noted, specialty brokers in hard markets differentiate by structuring programs with higher deductibles, captives, and data-driven risk improvement using telematics and AI dashcams to counter claims inflation and nuclear verdicts. That is not a generalist skillset.

Watch out for these red flags when evaluating brokers:

They can only offer quotes from one or two carriers.

They give vague answers about what bundling or telematics could save you.

They have no documented process for handling claims on your behalf.

They treat your renewal as a simple renewal rather than an opportunity to renegotiate.

They cannot explain FMCSA filing requirements in basic terms.

The motor carrier insurance guide is a useful reference when you are building your list of evaluation criteria and want to understand what full-service coverage programs should include.

A broker’s role: What most fleets overlook

Here is an honest observation from years of working in commercial trucking insurance: most fleets engage their broker intensely during the quote phase and then go quiet until the next renewal. That pattern leaves enormous value on the table.

The best broker relationships look more like an ongoing operational partnership. Proactive brokers schedule mid-year check-ins to review your loss runs, flag any new compliance requirements, and identify opportunities to improve your risk profile before the next renewal cycle starts. They run carrier negotiations based on your updated data, not just the previous year’s quote. They coach you on safety documentation that underwriters specifically reward.

Many fleets also underutilize broker expertise in claims advocacy. When a cargo claim or liability incident gets disputed, having a broker who knows how to communicate with the claims adjuster and push back on low settlement offers can make a five-figure difference in the outcome.

Choosing a specialty broker is not a one-time cost decision. It is a long-term strategic move that compounds over time as your loss history improves, your risk profile gets documented, and your relationship with specialty carriers deepens. The fleet insurance optimization strategies that deliver the biggest results are almost always broker-led, not self-directed.

Ready to strengthen your fleet’s insurance strategy?

Your fleet deserves more than a generic policy from a carrier that barely understands commercial trucking. The difference between an informed broker partnership and going it alone can run into tens of thousands of dollars per year in premiums, coverage gaps, and claims outcomes.

At Insuaria, we work directly with fleet operators and logistics managers to evaluate your current coverage, identify gaps, and structure programs that match your actual risk profile. Whether you run five trucks or five hundred, our team brings the specialized market access and compliance expertise your operation needs. Get a specialized broker consultation and see what purpose-built trucking coverage looks like. You can also explore our full range of insurance broker solutions for truck fleets to understand exactly how we approach fleet risk management.

Frequently asked questions

How can a broker help new trucking companies secure insurance?

Brokers access non-standard surplus lines markets when regular insurers decline, helping new authorities get required coverage including $1M liability and $100K cargo quickly, even in the first 12 months of operation. Without a broker, most new authorities face flat declines from standard carriers.

What savings can brokers help fleets achieve on insurance premiums?

Brokers can help fleets save 5 to 15% through bundling and an additional 15 to 25% when telematics risk programs are implemented and documented. These savings stack when combined with improved driver records and higher deductible structures.

What should I look for when choosing a trucking insurance broker?

Choose brokers with a dedicated trucking focus, broad carrier access including surplus lines markets, and proven expertise in risk management. Specialty brokers in hard markets structure programs with captives, higher deductibles, and data-driven tools that generalists cannot replicate.

How does a claim affect my future insurance premiums?

A single claim can trigger premium increases of $2,000 to $5,000 per year for three to five years after the incident, making claims prevention and management one of the highest-return investments in your fleet’s financial health.

Can technology like dashcams really lower my trucking insurance premiums?

Yes. Telematics and AI dashcam programs can reduce premiums by 15 to 25% when the data demonstrates consistent safe driving behavior. They also provide critical video evidence that strengthens your defense in contested liability claims.

Recommended

Comments