What is reinsurance in trucking: a guide for fleet managers

- Guyorguy Laguerre

- May 16

- 11 min read

TL;DR:

Reinsurance is insurance for insurers that helps trucking companies maintain coverage limits and stabilize premiums. Its market dynamics greatly influence freight insurance costs, capacity, and renewal conditions by transferring risk to specialized entities globally. Understanding reinsurance is essential for fleet managers to navigate market cycles, optimize renewal strategies, and ensure adequate coverage beyond federal minimums.

Most trucking company owners and fleet managers assume reinsurance is something only insurance executives worry about. It isn’t on the renewal checklist, nobody calls to sell it to you, and your broker has never explained it over coffee. But understanding what is reinsurance in trucking may be the single most useful thing you can do before your next policy renewal. Reinsurance is the hidden engine behind your insurance costs, your coverage limits, and whether your insurer even wants your business. When reinsurance markets tighten, your premiums go up, your options shrink, and your renewal gets harder. This guide explains exactly why.

Table of Contents

What is reinsurance in trucking and why does it matter for your fleet?

The link between reinsurance and trucking insurance market dynamics

Reinsurance’s role in meeting FMCSA insurance minimums and managing catastrophic risk

Alternative market structures: risk retention groups and their use of reinsurance

The uncomfortable truth about reinsurance and trucking insurance

Key Takeaways

Point | Details |

Reinsurance fundamentals | Reinsurance is insurance for insurers, allowing them to manage risk and maintain capacity in trucking markets. |

Contract types | Treaty and facultative reinsurance vary in scope and underwriting, impacting coverage and risk transfer. |

Market influence | Reinsurance costs and availability directly affect trucking insurance pricing, underwriting, and capacity. |

Compliance and risk | Reinsurance supports insurers in meeting FMCSA minimums and covering catastrophic trucking risks. |

Strategic renewal planning | Understanding reinsurance cycles helps fleet managers anticipate underwriting changes at insurance renewal. |

What is reinsurance in trucking and why does it matter for your fleet?

Reinsurance is, at its core, insurance for insurers. When your trucking company buys a liability policy, your insurer absorbs the financial risk of paying claims. But insurers don’t keep all that risk sitting on their books. They transfer a portion of it to a reinsurer, a specialized financial entity that agrees to cover losses above a certain threshold in exchange for a share of the premium. The trucking insurer in this arrangement is called the ceding company.

Why does this matter to you? Because the trucking industry is one of the riskiest sectors for insurers to underwrite. A single catastrophic accident involving a fully loaded semi can generate a $10 million or $20 million claim. Without reinsurance, most insurers couldn’t afford to write trucking policies at all. The risk concentration would be too dangerous.

Reinsurance protects trucking insurers from volatility and financial strain. When losses pile up after a bad quarter of highway accidents, the reinsurer absorbs the overflow. This keeps your insurer solvent, willing to renew your policy, and financially able to pay claims. Without that backstop, smaller and mid-size trucking insurers would face existential risk after any severe loss year.

Here’s what reinsurance does for the trucking insurance market specifically:

Enables insurers to write higher coverage limits than their capital base would otherwise support

Stabilizes year-over-year underwriting results, which controls how wildly premiums swing

Gives insurers confidence to cover large fleets with complex risk profiles

Supports the availability of commercial trucking insurance for operators who would otherwise be uninsurable

Spreads catastrophic loss risk globally across multiple reinsurance entities

“Reinsurance is insurance for insurance companies: a trucking insurer transfers part of its liability risk to a reinsurer, so the insurer can reduce volatility and protect solvency while keeping capacity to underwrite trucking business.” — Evolum

The practical implication for fleet managers is this: the health of the reinsurance market upstream is directly connected to whether your renewal goes smoothly or becomes a crisis.

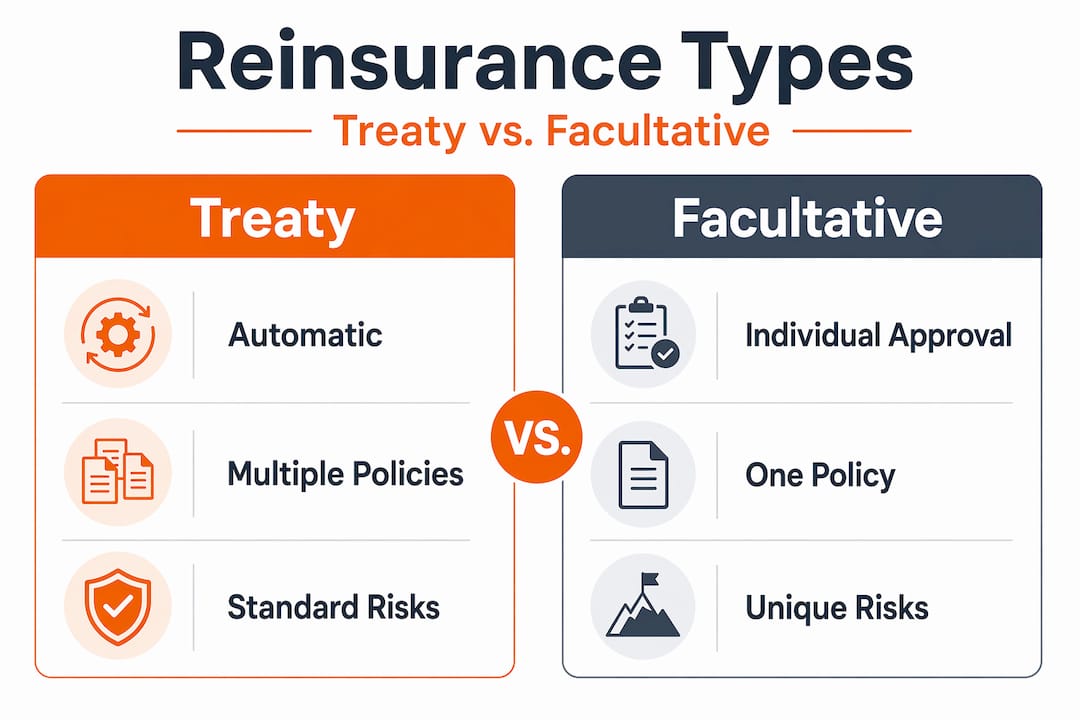

How reinsurance contracts work: treaty versus facultative

There are two main types of reinsurance arrangements, and understanding their differences helps explain why some trucking insurers can handle large fleets while others cap out at 10 or 20 power units.

Treaty reinsurance covers a broad class of policies automatically. If your insurer has a treaty in place, every trucking policy they write up to a certain profile gets reinsurance coverage without individual negotiation. This is the most common structure for standard commercial trucking risks.

Facultative reinsurance works differently. It covers individual policies or unusual risks that fall outside treaty parameters. If you operate an oversized load fleet hauling hazardous materials across state lines, your insurer might need to seek facultative reinsurance specifically for your account. This takes more time and typically costs more.

Here’s how the two structures compare:

Feature | Treaty reinsurance | Facultative reinsurance |

Coverage trigger | Automatic for qualifying policies | Negotiated per individual policy |

Speed of placement | Fast, already in place | Slower, requires separate negotiation |

Best for | Standard trucking risks | Unusual or high-limit risks |

Insurer flexibility | High for routine renewals | Limited, case-by-case basis |

Impact on your renewal | Smooth if you fit criteria | Possible delays or coverage gaps |

Insurers often layer both treaty and facultative arrangements. A carrier might use a treaty to cover the first $2 million of liability across all policies, then add facultative coverage above that for specific high-limit accounts. The sequencing matters because it determines exactly when the reinsurer’s obligation kicks in.

The legal structure backing all of this is important: reinsurance is contract-based indemnification that is only payable after the ceding insurer has paid losses under its own policy. In other words, the reinsurer doesn’t step in until your primary insurer has already paid. This sequencing reinforces why your primary insurer’s financial health matters, not just the reinsurer’s.

Understanding these contract types gives fleet managers a useful mental model for understanding what happens with commercial auto insurance limits. When an insurer tells you they can’t offer the coverage limit you need, it often means their reinsurance treaty doesn’t support it for your risk class.

Identify whether your insurer uses treaty or facultative structures for your risk profile

Ask your broker whether your account fits standard treaty criteria or requires individual negotiation

If facultative placement is needed, build extra lead time into your renewal timeline

Understand that changes in reinsurance terms at treaty renewal (often January 1 each year) can affect your coverage mid-cycle

Request transparency from your broker about how your insurer secures reinsurance backing

The link between reinsurance and trucking insurance market dynamics

Here’s the part that directly hits your renewal invoice. When reinsurers decide that trucking is too costly to support at current prices, they raise their rates, add exclusions, or reduce the limits they’ll cover. Your insurance company absorbs those increased costs, and they don’t quietly eat them. They pass them to you.

Rising reinsurance costs lead directly to higher trucking premiums, higher minimum deductibles, and stricter underwriting requirements. Insurers start demanding cleaner loss histories. They stop writing accounts with certain commodities or route types. They reduce the maximum fleets they’ll quote. From your seat, this looks like the market getting harder. The actual cause is upstream.

The data backing this up is grim. Commercial auto liability has been unprofitable for insurers for 14 consecutive years, and insurance costs per mile reached $0.102 in 2024. That sustained unprofitability forces reinsurers to reprice their exposure, which cascades down to the fleet manager receiving a 25% renewal increase letter.

The domino effect looks like this:

Reinsurers experience poor results from trucking-related claims

Reinsurers raise their own premiums and tighten terms at treaty renewal

Primary trucking insurers face higher costs and reduced capacity from reinsurers

Insurers pass costs through, cut capacity, or exit the market entirely

Fewer insurers compete for your business, pushing prices higher

Fleets with any loss history face the steepest rate increases or non-renewals

Pro Tip: Track the reinsurance market cycle, not just your own loss runs. If January reinsurance treaty renewals were difficult industrywide, expect your summer or fall renewal to feel the effects regardless of how clean your fleet’s record is.

The reinsurance cycle also creates windows of opportunity. When reinsurers return to profitability and inject fresh capacity into the market, insurers become more competitive, willing to write more business at lower rates. Fleet managers who understand this cycle can time shopping their coverage strategically rather than reactively.

The most important thing to recognize: your insurance costs are not set solely by your own driving record or claims history. They are also shaped by a global risk market pricing in accidents, lawsuits, jury verdicts, and natural disasters that have nothing to do with your fleet. Understanding this helps you reduce trucking insurance costs by focusing on the variables you can actually control, like driver safety programs, telematics, and claims management, rather than being blindsided by market forces.

Reinsurance’s role in meeting FMCSA insurance minimums and managing catastrophic risk

Federal minimum insurance requirements exist to protect the public from uninsured trucking losses. But those minimums were established years ago, and the cost of catastrophic accidents has increased significantly since then.

Here’s what FMCSA currently requires as minimum liability limits:

Carrier type | Commodity | FMCSA minimum |

For-hire interstate | General freight (under 10,001 lbs) | $300,000 |

For-hire interstate | General freight (over 10,001 lbs) | $750,000 |

For-hire interstate | Hazardous materials (certain classes) | $1,000,000 to $5,000,000 |

For-hire interstate | Household goods | $300,000 |

The problem is that a single serious injury accident, particularly one involving a fatality or permanent disability, can easily generate claims that exceed $750,000. Trial verdicts in trucking accidents have been climbing for years, with nuclear verdicts (jury awards exceeding $10 million) becoming more common. FMCSA’s minimum thresholds often fall short for catastrophic losses, which is precisely why insurers depend on reinsurance-backed capacity to write higher limits.

Without reinsurance, an insurer couldn’t safely offer a $5 million liability policy to a 50-truck fleet. The potential for a single event to wipe out years of premium income is too high. Reinsurance enables the insurer to offer limits that actually protect your business against real-world exposure, not just the federal floor.

Pro Tip: Treating FMCSA minimums as a coverage target rather than a floor is one of the most expensive mistakes a fleet owner can make. Work with a licensed insurance professional to assess your actual exposure based on routes, cargo, fleet size, and litigation environment in the states you operate. Consider fleet insurance coverages that exceed federal minimums by a meaningful margin.

The reinsurance benefits in trucking become most visible at the catastrophic end of the loss spectrum. When a severe accident generates a claim that exceeds your insurer’s retention threshold, the reinsurer steps in. Without that mechanism, insurers would set policy limits conservatively low, leaving fleets exposed.

Alternative market structures: risk retention groups and their use of reinsurance

Some fleet managers, particularly those frustrated with the hard commercial market, look at alternative insurance structures. Risk retention groups (RRGs) are one option worth understanding, largely because their business model depends heavily on reinsurance.

An RRG is a liability insurance company owned and controlled by its members, who share similar or related liability exposures. In trucking, an RRG might be formed by a group of motor carriers who pool their risk rather than buying coverage from a traditional insurer. The appeal is potential cost savings and more direct control over the insurance program.

Here’s what distinguishes RRGs from traditional trucking insurers:

Members are both the insured and the owners of the insuring entity

RRGs are chartered in one state but can operate nationally under the Liability Risk Retention Act

They are typically more specialized, focusing on specific industry segments like trucking

Underwriting decisions tend to favor member safety culture and loss control

Surplus and dividends can return to members when loss ratios are favorable

The financial backbone of most RRGs is reinsurance. Risk retention groups obtain reinsurance to increase their claims-paying capacity, and state domicile regulators often require it as a condition of licensure. This mandatory reinsurance acts as a deep-pocket backstop, ensuring that even if member losses spike, the RRG can pay claims without becoming insolvent.

“Almost all risk retention groups are required to carry reinsurance by their state domicile to multiply their ability to cover claims and handle losses.” — National Risk Retention Association

For fleet managers considering an RRG, the reinsurance structure matters for evaluating the financial strength of the entity. Ask about the reinsurers backing the RRG, their ratings, and what the retention thresholds look like. A well-structured RRG with rated reinsurance behind it can be a legitimate alternative to the standard market. Refer to the full motor carrier insurance guide for a deeper look at the coverage structures available to operators.

The reinsurance policies for trucking entities, whether traditional carriers or RRGs, ultimately determine how much capacity exists in the market at any given time. When reinsurers retract, both traditional and alternative market options tighten simultaneously.

The uncomfortable truth about reinsurance and trucking insurance

After years of watching trucking companies struggle with renewal surprises, there’s a pattern worth naming directly: most fleet managers treat insurance as a commodity purchase rather than a risk finance decision. They shop purely on price, change carriers frequently for marginal savings, and view insurance as an unavoidable expense to be minimized. Reinsurance dynamics reveal why that approach is flawed.

Here’s the reality. The trucking insurance market is not a simple competitive market where lower price equals better deal. It is a layered system of risk transfer where the price you pay is partly determined by global capital markets, catastrophic loss trends, courtroom jury behavior, and reinsurer appetite in Zurich or London. None of those factors respond to your competitive bids.

What does respond to your actions is your risk profile. Reinsurers and insurers both analyze loss development, driver behavior data, fleet age, safety programs, and claims management quality. Fleets that invest in telematics, rigorous driver training, and proactive claims handling actually do get better treatment in a hard market, because their risk profile signals lower reinsurance exposure to the underwriter.

The fleet manager who understands reinsurance stops asking “why did my rate go up” and starts asking “what does my insurer need to see from me to get favorable treatment at their next reinsurance negotiation.” That’s a fundamentally more powerful position. Your safety investment is not just reducing accidents. It is improving your insurer’s reinsurance case for your account, which translates directly to pricing.

Understanding reinsurance in freight also clarifies why switching insurers in a hard market rarely solves the problem. The reinsurance market affects all carriers simultaneously. Shopping your account helps only if your risk profile genuinely merits better treatment. Otherwise, you’re moving from one tight market to another, spending time and relationship capital for no sustainable gain.

Ready to organize your trucking insurance review?

Understanding what is reinsurance in trucking is genuinely useful, but the next step is making sure your coverage position matches the realities of the current market. Reinsurance-driven changes in insurer appetite mean your existing policy may no longer reflect what you actually need.

Insuaria helps trucking business owners and fleet managers organize the information licensed insurance professionals need to review their coverage. Through simple intake forms, you can submit your fleet details, coverage history, and operational profile so that a licensed agency partner can follow up with relevant guidance. Insuaria does not provide insurance advice or bind coverage. We simply make the first step of the process easier, faster, and more organized. Start your trucking insurance intake today and give your next renewal the preparation it actually deserves.

Frequently asked questions

What exactly is reinsurance and how does it affect my trucking insurance?

Reinsurance is the mechanism by which insurance companies transfer risk to specialized financial entities to protect their solvency and maintain underwriting capacity. It affects your trucking insurance by shaping what coverage limits are available, how strictly underwriters review your account, and how much premium you ultimately pay.

Do trucking fleets deal directly with reinsurance?

No. Fleets do not purchase reinsurance themselves. Reinsurance pays after the insurer pays, so it operates entirely between your insurer and the reinsurer. You benefit from its stabilizing effect without ever interacting with the reinsurer directly.

Why are FMCSA minimum insurance requirements sometimes insufficient?

Current federal minimums fail to adequately cover catastrophic crashes, particularly as medical costs and jury awards have increased significantly since those thresholds were set. Insurers rely on reinsurance-backed capacity to offer limits that reflect actual catastrophic exposure rather than the regulatory floor.

How can understanding reinsurance help with managing insurance renewals?

Knowing that reinsurance renewals influence carrier behavior and underwriting appetite helps you anticipate stricter requirements or premium increases that have nothing to do with your own loss history. It allows proactive renewal planning rather than reactive scrambling when your broker delivers bad news.

What role do risk retention groups play in trucking insurance?

Risk retention groups are member-owned alternative market insurers that use reinsurance to multiply their claims-paying capacity. State domiciles typically require RRGs to carry reinsurance, making them a financially backed alternative for fleets where conventional insurers have reduced appetite or capacity.

Recommended

Comments