Trucking insurance renewal: A step-by-step guide for fleet owners

- Guyorguy Laguerre

- May 3

- 12 min read

TL;DR:

Maintaining continuous insurance coverage is crucial to preserve trucking operating authority and avoid disruptions.

Preparing and organizing renewal documents 60-90 days in advance helps prevent lapses and ensures smooth renewal.

Active safety management, technology use, and organized documentation lead to better insurance rates and operational stability.

Your operating authority can vanish overnight. Not because of an accident, not because of a failed inspection, but because your insurance lapsed. For FMCSA-regulated interstate carriers, continuous coverage is mandatory, and a single missed filing or renewal gap triggers authority revocation. That means trucks sit idle, loads get cancelled, and revenue stops while you scramble to refile. The good news is that a well-organized renewal process eliminates that risk entirely. This guide walks you through every stage, from foundational regulations to post-renewal monitoring, so your fleet stays moving and your business stays protected.

Table of Contents

Key Takeaways

Point | Details |

Compliance is critical | Failing to renew on time instantly revokes operating authority and threatens revenue. |

Preparation prevents mistakes | Organizing documents and following deadlines avoids costly lapses and late fees. |

Technology lowers premiums | Sharing safety data from dashcams and ELDs can earn discounts and reduce risk. |

Cash flow tools help | Financing and staggered premiums make renewal affordable and prevent coverage gaps. |

Strategic renewals pay off | Using renewal as a chance to optimize coverage creates savings and long-term compliance. |

Understanding trucking insurance renewal: Key concepts and regulations

Before you can manage the renewal process effectively, you need to know why it matters beyond just writing a check every year. Trucking insurance renewal is not a passive administrative task. It is an active compliance obligation with real consequences for your operating authority, your revenue, and your liability exposure.

The FMCSA continuous coverage requirement

The Federal Motor Carrier Safety Administration (FMCSA) requires interstate carriers to maintain continuous proof of insurance on file. When your insurer submits an update to a form like the BMC-91X through the FMCSA portal, it signals that your coverage is active. If that proof lapses, even briefly, the FMCSA can revoke your operating authority. Reinstating it requires refiling paperwork, paying fees, and waiting through processing times. You cannot haul freight during that window. Understanding truck insurance basics is the starting point for building a renewal process that keeps your authority intact.

What renewal actually costs in 2026

Trucking insurance is not cheap, and it is getting more expensive. Commercial truck insurance averages $0.102 per mile based on 2024 ATRI data, with owner-operators typically paying between $900 and $1,800 per month. Carriers with new authority face significantly steeper rates, often between $1,800 and $2,500 per month or higher, reflecting the 40 to 100 percent premium over established fleets. In 2025 and into 2026, liability rates increased 7 to 20 percent, driven largely by nuclear verdicts (jury awards exceeding $10 million) and broader litigation trends in the trucking industry.

These numbers matter because they shape how you plan your cash flow, how you compare quotes, and how much leverage organized documentation gives you when your insurer reviews your risk profile.

Rate drivers you need to understand

Factor | Effect on premium |

Nuclear verdicts and litigation trends | Pushes liability rates 7 to 20% higher |

New authority (under 2 years) | Adds 40 to 100% to base rates |

Poor CSA/SMS safety scores | Direct premium increases from insurers |

Unresolved claims or loss history | Signals high risk, raises rates significantly |

Technology adoption (AI dashcams, ELDs) | Can offset increases through demonstrated risk reduction |

Understanding these drivers means you can take targeted action before renewal rather than just accepting whatever rate your insurer offers. The difference between a reactive carrier and a prepared one is often thousands of dollars per year.

Preparing for renewal: Documents, deadlines, and prerequisites

Preparation is where most fleet owners either succeed or stumble. The renewal process does not start a week before your policy expiration. It starts 60 to 90 days out, giving you enough time to gather documentation, address compliance issues, and evaluate your coverage needs without pressure.

Core documents you need to collect

Here is a practical checklist of what most insurers and FMCSA compliance requirements will ask for during renewal:

Current vehicle list including VIN numbers, year, make, model, and gross vehicle weight rating for each unit

Driver records including MVR (Motor Vehicle Records) for all drivers, CDL copies, and any accident or violation history

Loss run reports from your current insurer covering at least three to five years of claims history

Prior carrier proof of coverage showing no lapses in your insurance history

FMCSA compliance documentation including your current MC number, USDOT number, and operating authority certificate

CSA/SMS score reports pulled from the FMCSA Safety Management System portal

Cargo and freight classifications that reflect your actual haul types, since misclassified cargo can void coverage

Missing any of these at submission time delays the review process and can push your renewal past your expiration date. Reviewing insurance tips for trucking companies before you begin gathering documents helps you spot gaps early.

Timelines that prevent gaps in coverage

Most insurers need 30 to 45 days to fully process a commercial trucking renewal, especially for fleets with complex risk profiles. Build your schedule backward from your expiration date:

90 days out: Pull loss runs, check CSA scores, audit your vehicle and driver lists

60 days out: Contact your current insurer or begin shopping for alternative coverage

45 days out: Submit all documentation packages to your insurer or broker

30 days out: Confirm receipt, review coverage terms, and address any flagged items

15 days out: Confirm FMCSA filings are current and renewal is confirmed in writing

Expiration date: Policy renews without interruption

New carriers face 18 months of FMCSA monitoring with stricter scrutiny, which means insurers are paying closer attention to your safety record during that period. If you are still in that window, start the renewal process even earlier and make sure your documentation is spotless.

Managing lump-sum premium payments

One of the most overlooked renewal risks is cash flow. Annual or semi-annual premium payments are a significant lump sum, and if your accounts receivable are slow, you may find yourself unable to pay on time. That gap can cause a lapse. Understanding trucking insurance premiums in detail helps you anticipate the payment structure and plan ahead.

Financing solutions exist specifically for commercial trucking premiums. Some insurers offer monthly installment plans directly. Third-party premium financing companies provide short-term loans that let you spread the cost across 10 to 12 months. If you are hauling for a larger carrier, ask whether they offer insurance programs through their fleet agreement.

Pro Tip: Pull your CSA scores from the FMCSA SMS portal at least 90 days before renewal. If any category is approaching the intervention threshold, address it before your insurer runs their own check. Carriers with scores above threshold in categories like unsafe driving or hours of service violations routinely see premium increases of 10 to 25 percent at renewal, sometimes more.

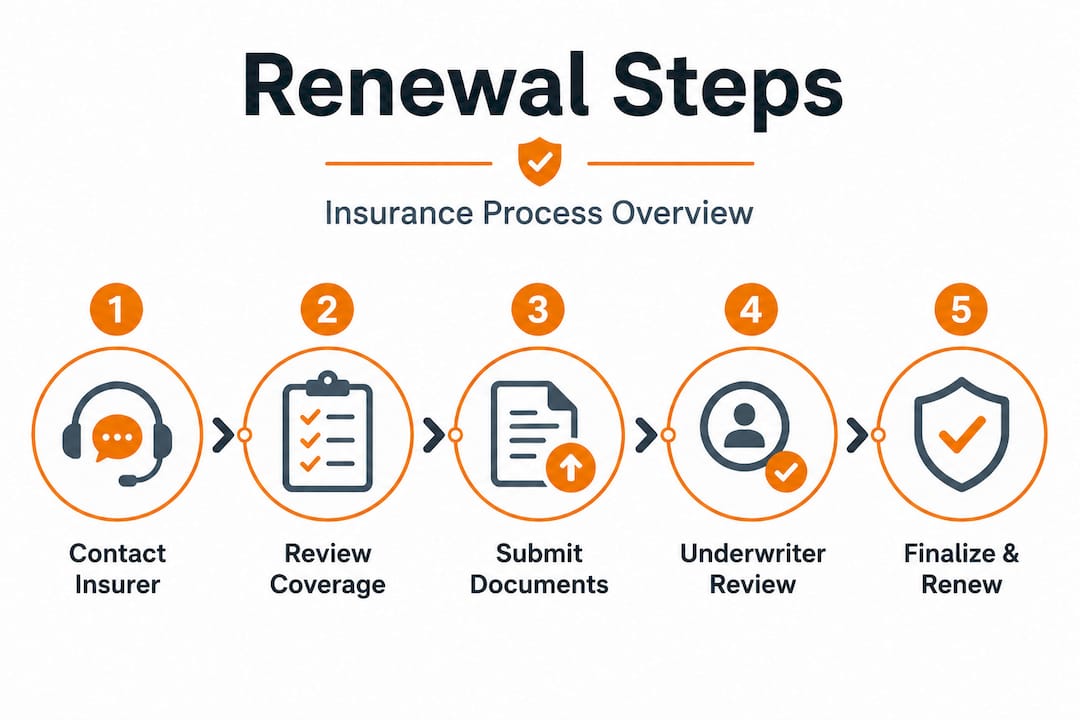

Step-by-step renewal process for trucking insurance

With your documents assembled and your timeline set, here is exactly how to move through the renewal process from start to finish.

Step 1: Initiate contact with your current insurer

Do not wait for your insurer to reach out. Contact them directly 60 to 90 days before expiration and confirm that your account is flagged for renewal. Ask for a list of any additional documentation they will need based on your fleet’s current configuration. If you have added vehicles, changed cargo types, or hired new drivers since the last renewal, flag those changes immediately.

Step 2: Review your current coverage and identify gaps

Renewal is the right moment to ask whether your current coverage still matches your actual risk exposure. Has your fleet grown? Are you hauling more hazardous materials than before? Are there routes you now service that cross into higher-risk zones? Reviewing truck insurance confidence resources gives you a framework for evaluating whether your existing policy structure still fits.

Step 3: Submit your documentation package

Gather everything on your checklist and submit it as a single organized package. Disorganized submissions slow down insurer review and create opportunities for things to get missed. If you are working with a broker, truck insurance brokers can often facilitate this submission process and flag documentation gaps before they cause delays.

Step 4: Insurer evaluates your application

During this phase, the underwriter reviews your loss runs, CSA scores, driver records, and vehicle list to assess your risk profile. They may come back with questions or requests for additional documentation. Respond promptly. Delays here push your renewal date closer to your expiration and increase stress on your timeline.

Step 5: Address flagged risks and finalize coverage

If the underwriter flags anything, whether it is a specific driver’s violation history, a high-value vehicle with no prior loss data, or a cargo type they are not comfortable with, you need to respond with documentation or propose solutions. This might mean removing a driver from your policy, adding a coverage endorsement, or adjusting limits. Fleet insurance cost strategies offer concrete approaches for negotiating these adjustments without inflating your total premium.

Step 6: Confirm FMCSA filing and premium payment

Once the coverage is finalized, confirm that your insurer has submitted the necessary proof of coverage to the FMCSA portal. Do not assume this happened. Log into your FMCSA account and verify that your filing status shows as active before your current policy expires.

Warning: A policy lapse, even for a single day, can instantly halt your operating authority. The FMCSA does not offer a grace period. If your insurer’s filing is even slightly delayed, your authority goes dark and you cannot legally haul freight until coverage is confirmed and the filing is reprocessed.

Pro Tip: Ask your insurer to provide written confirmation of the FMCSA filing date and reference number every renewal cycle. Keep this on file. If there is ever a dispute about a coverage gap, this documentation is your first line of defense.

Troubleshooting and avoiding common renewal mistakes

Even organized fleet owners run into problems. Here is how to identify and fix the most common renewal issues before they become costly disruptions.

The most common renewal mistakes

Submitting incomplete documentation causes underwriter delays and often results in a coverage gap if the review is not finished before expiration

Missing the renewal initiation window by waiting until 30 days or less before expiration gives you almost no time to resolve problems

Failing to update vehicle and driver lists means your coverage may not reflect your actual fleet, which can create claims denial scenarios

Ignoring CSA score deterioration between renewals often results in rate shock when the new premium arrives

Not confirming FMCSA filings after the renewal is processed leaves you vulnerable to lapses you are not even aware of

Poor CSA scores directly hike premiums in ways that compound over time. A carrier that ignores a borderline SMS score for 12 months may face a 20 to 30 percent rate increase at the next renewal cycle, on top of whatever market-wide increases apply.

Technology as a risk management tool

This is an area where proactive fleets consistently separate themselves from reactive ones. AI-powered dashcams and electronic logging devices (ELDs) do more than record data. They demonstrate to insurers that your fleet operates with active safety oversight. Some insurers now offer documented insurance cost reduction discounts specifically for fleets that share dashcam and ELD data as part of their risk profile submission.

Installing these systems mid-policy year gives you data to present at renewal. A six to twelve month record of safe driving behavior, clean hours-of-service logs, and no hard-braking events is a concrete, quantifiable argument for a lower rate.

Pro Tip: Keep a log of every communication with your insurer and broker throughout the renewal process. Note the date, the person you spoke with, and what was discussed or confirmed. If a filing gets delayed or a document gets lost, your communication log is the fastest way to identify where the breakdown happened and get it corrected.

What to expect after renewal: Monitoring compliance and optimizing costs

Renewing your policy is not the end of the process. For new carriers especially, the 18-month FMCSA monitoring period means your compliance performance continues to affect your insurability and rates throughout the year. But even established carriers benefit from active post-renewal management.

Post-renewal monitoring checklist

Confirm your FMCSA authority status is active and shows current coverage

Set a calendar reminder for 90 days before your next renewal date

Schedule quarterly CSA score reviews to catch any deteriorating categories early

Update your vehicle and driver lists immediately whenever changes occur, not just at renewal

Review your cargo classifications if your haul types shift during the year

Fleets that adopt technology like AI dashcams and ELDs and share that data with insurers are increasingly being rewarded in a hard market. Hard markets favor prepared low-risk profiles, meaning the fleets with the cleanest safety records, the most organized documentation, and the most demonstrable risk management practices get better access to coverage and more competitive rates.

Adjusting coverage as your business changes

A policy that fit your fleet perfectly at renewal may not fit it six months later if you have added three trucks, hired four new drivers, or started hauling a new cargo type. Most insurers allow mid-term policy endorsements to reflect these changes. Make them proactively rather than discovering the gap after a claim is filed.

A mid-year review with your broker or licensed insurance professional takes 30 to 60 minutes and can prevent a coverage denial that would cost you far more. Think of it as a compliance audit you schedule on your own terms rather than one that happens during a claim.

Pro Tip: Schedule your annual renewal review reminder at the same time you complete each renewal. When renewal is fresh in your mind, set the calendar event for 90 days before next year’s expiration date. Pair it with a reminder to pull CSA scores and run a quick vehicle and driver audit. This single habit eliminates the scramble that causes most renewal problems.

Expert perspective: Prepared fleets win in tough insurance markets

Here is something worth saying plainly: most trucking businesses treat insurance renewal as a chore, and the insurance market treats them accordingly.

The carriers that consistently secure the best rates, even in a hard market where liability rates are climbing 7 to 20 percent annually, are not just lucky. They operate differently. They monitor their CSA scores quarterly. They invest in technology that generates data, not just because regulators might ask for it, but because that data is a negotiating tool. They submit renewal documentation that is clean, complete, and early. And they build relationships with licensed insurance professionals who advocate for them at underwriting.

Technology adoption combined with organized documentation is the single most effective counter to a hard insurance market. Nuclear verdicts are driving up baseline liability rates across the industry, and there is nothing an individual fleet owner can do about that. But your relative risk profile is entirely within your control. An insurer looking at two fleets with similar size and haul types will price the one with better documentation, cleaner records, and demonstrable safety technology more favorably every time.

The mindset shift that matters most is this: renewal is not an obligation you fulfill once a year. It is a continuous process of building and maintaining a risk profile that works in your favor. The proven cost-reduction strategies that high-performing fleets use are not secrets. They are just disciplined habits that most carriers skip because the payoff is not immediate.

Start treating your insurance renewal as a strategic asset rather than an administrative box to check. The fleets that do this consistently outperform the ones that scramble every year, not just on insurance costs, but on overall operational stability.

Upgrade your renewal process with Insuaria solutions

Getting your renewal documentation organized is the hardest part for most fleet owners, and it is also where most costly mistakes happen.

Insuaria’s intake platform is built specifically for trucking businesses preparing for insurance review. You can use the business insurance intake tool to organize your fleet details, coverage history, and compliance documents in one place before a licensed agency partner reviews your submission. If you are looking for truck coverage options, the truck insurance intake form walks you through the information licensed professionals need to evaluate your situation. And if you need to share documents securely with your broker or agent, Insuaria’s secure file sharing feature makes that process fast and organized. Insuaria does not bind coverage or provide insurance advice. Its role is to help you show up to the renewal conversation prepared, organized, and ready.

Frequently asked questions

What documents are required for trucking insurance renewal?

You need vehicle lists, driver records, loss run reports, prior carrier proof of coverage, and any FMCSA compliance forms relevant to your operating authority. New carriers under FMCSA monitoring should also include CSA score reports and any safety improvement documentation.

What happens if I miss the insurance renewal deadline?

Missing the deadline can revoke your FMCSA operating authority and halt all operations until you refile and regain coverage. Lapses revoke operating authority and require a full refiling process before you can legally haul freight again.

How can I reduce trucking insurance premium increases during renewal?

Maintain low CSA and SMS scores, adopt technology like AI dashcams and ELDs, and keep all documentation organized for insurer review. Fleets sharing safety data with insurers are consistently rewarded with better rates even in a hard market.

What cash flow options are available for lump-sum insurance payments?

Financing solutions and staggered payment plans can help manage large annual premiums to avoid gaps in coverage. Premium financing options from third-party lenders or directly through some insurers spread the cost across 10 to 12 monthly payments.

Recommended

Comments