Why Choose Tailored Fleet Policies for Your Business

- Guyorguy Laguerre

- 2 days ago

- 10 min read

TL;DR:

Tailored fleet policies are customized insurance programs based on a fleet’s specific risks, operational needs, and vehicle profiles. They offer significant cost savings through consolidation, accurate risk alignment, and operational flexibility, surpassing standard policies that rely on generic categories. These programs address federal minimum coverage gaps by setting limits aligned with current liabilities and provide dynamic adjustments for seasonal and operational changes.

Tailored fleet policies are specialized commercial insurance programs built around the specific risk profile, vehicle mix, and operational demands of an individual fleet business. Unlike off-the-shelf commercial auto coverage, these programs align deductibles, liability limits, and endorsements to what your fleet actually does, not what a generic underwriting template assumes. Fleet managers who consolidate vehicles under a single customized policy can save 10% to 25% per vehicle compared to insuring each unit separately. That figure climbs to 15% to 40% in total savings when deductible optimization, telematics data, and annual carrier shopping are layered together. Agencies like First Heritage Insurance Agency and JG Parker Insurance Associates, along with federal regulators at FMCSA, have all documented why standard minimums and generic policies leave fleets financially exposed.

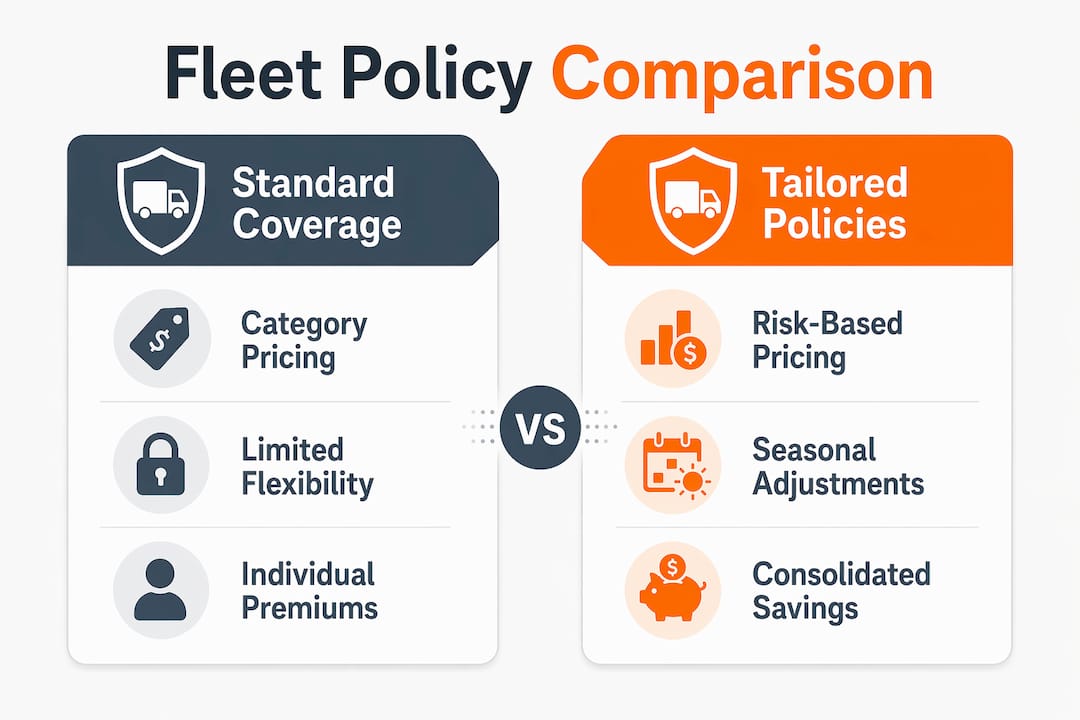

Why choose tailored fleet policies over standard coverage?

The core argument for customized fleet policies is simple: standard commercial auto coverage prices risk by category, not by your actual operation. A generic policy treats a refrigerated grocery fleet the same as a construction materials hauler. Your premiums, deductibles, and liability limits reflect an average, not your reality.

Financial savings through consolidation

Placing all vehicles under one fleet policy triggers volume discounts that individual vehicle policies cannot match. Carriers reward consolidated accounts because they reduce administrative overhead and provide a more complete picture of fleet risk. When you add deductible optimization to that base, reducing premiums by 15% to 35% becomes achievable by simply adjusting physical damage deductibles upward. That is not a minor line-item adjustment. For a fleet spending $200,000 annually on insurance, a 25% reduction is $50,000 back in operating capital.

Risk alignment and coverage accuracy

Generic policies create two problems simultaneously: they overcharge for risks you do not carry and underprotect against risks you do. A tailored program uses actual operational data, including SAFER scores, CSA percentiles, driver records, and cargo classifications, to align underwriting inputs to your risk profile. This produces more accurate pricing and eliminates the coverage gaps that surface only after a claim is filed. For fleet managers, that precision is the difference between a manageable loss event and a catastrophic one.

Operational flexibility and seasonal adjustments

Seasonal fleets face a specific problem: paying full premiums during off-peak months for coverage they are not using. Tailored programs solve this by adjusting liability limits and deductibles ahead of peak operational periods. Endorsements for temporary leased units and seasonal drivers can be added and removed without triggering a full policy rewrite. This flexibility is a direct cost control lever that standard policies simply do not offer.

Driver safety integration and telematics

Telematics data from systems like Samsara, Verizon Connect, or Motive gives carriers hard evidence of driver behavior. Tailored fleet policies integrate telematics and driver safety data as underwriting inputs, which means a fleet with strong safety scores can negotiate meaningfully lower premiums. The inverse is also true: telematics data that reveals high-risk behavior gives you the information to intervene before a claim occurs, not after.

How do tailored fleet policies differ from standard commercial auto coverage?

The structural differences between tailored fleet programs and standard commercial auto policies go beyond price. They affect how coverage responds during rapid growth, how claims are processed, and how much administrative burden falls on your operations team.

Scheduled vs. blanket fleet policies

Two primary fleet policy structures exist: scheduled and blanket. A scheduled fleet policy lists every vehicle by VIN and requires a policy update each time a vehicle is added, traded, or retired. This creates a real operational risk. If a new truck hits the road before the paperwork is processed, it may be uninsured. A blanket fleet policy covers all vehicles meeting a defined description, with mid-term additions handled through periodic audits rather than individual endorsements. Mid-to-large fleets strongly prefer blanket structures because they eliminate the uninsured gap risk that scheduled policies create during rapid scaling.

Risk-based underwriting vs. category pricing

Standard commercial auto policies price by vehicle class and use type. Tailored fleet underwriting goes deeper. Carriers examine loss history, driver qualification files, maintenance records, and safety program documentation. A fleet with three years of clean loss history and a documented driver training program will receive materially different terms than one with identical vehicles but no safety infrastructure. The difference is not cosmetic. It affects both premium and the breadth of coverage available.

Feature | Standard commercial auto | Tailored fleet policy |

Vehicle additions | Requires individual endorsement | Covered under blanket audit cycle |

Pricing basis | Vehicle class and use type | Actual loss history, safety scores, cargo type |

Deductible flexibility | Limited, preset tiers | Customizable by coverage line |

Seasonal adjustments | Not available | Available via endorsement |

Telematics integration | Rarely used | Standard underwriting input |

Compliance filings | Manual, policy by policy | Managed centrally under one policy |

Pro Tip: If your fleet adds more than four vehicles per year, a blanket policy structure almost always reduces both administrative cost and coverage gap risk compared to a scheduled policy.

What practical strategies optimize a tailored fleet insurance policy?

Knowing why tailored fleet policies matter is one thing. Knowing how to build and maintain one that actually performs is another. The following strategies reflect what experienced fleet operators and specialized brokers consistently apply.

Consolidate all vehicles under a single policy. The volume discount logic is straightforward: more vehicles mean more premium, and more premium means more negotiating leverage. Carriers compete harder for larger accounts. Consolidation also simplifies claims management, renewals, and compliance filings. Review your fleet insurance coverage structure annually to confirm all units are captured under one program.

Optimize deductibles based on claim frequency and cash flow. Moving to higher deductibles shifts small claim costs in-house and lowers baseline premiums significantly. This is a strategic decision, not just a coverage selection. A fleet with strong cash reserves and low claim frequency should carry higher deductibles. A fleet with thin margins and frequent minor incidents should carry lower ones. Match the deductible structure to your actual financial position, not an arbitrary default.

Adjust coverage ahead of known operational changes. If you add seasonal drivers in Q4, expand into a new cargo category, or lease additional units for a contract, update your policy before those changes take effect. JG Parker Insurance Associates documents that proactive coverage adjustments for seasonal peaks prevent both overpayment during slow periods and underinsurance during high-exposure periods.

Use telematics data as a negotiating tool. Carriers respond to evidence. If your Samsara or Verizon Connect data shows hard-braking events declining 30% year over year, bring that to your renewal conversation. Telematics-backed safety improvements are one of the few areas where you can directly influence your own premium outside of loss history.

Shop carriers annually. Carrier pricing appetite shifts every year based on their own loss experience, reinsurance costs, and market strategy. Annual carrier shopping produces 10% to 30% savings by targeting underwriters who are actively competing for your fleet class. Loyalty to a single carrier without market testing is a cost you are choosing to absorb.

Work with a broker who specializes in fleet underwriting. A generalist broker will place your fleet with whoever they know. A specialist broker knows which carriers have appetite for your specific cargo type, safety profile, and fleet size. The difference in terms and pricing can be substantial. Learn more about how specialized brokers approach fleet accounts differently than standard commercial lines producers.

Pro Tip: Request a loss run report covering at least three years before your renewal. Carriers use this data to price your policy. Reviewing it yourself lets you identify patterns and address them proactively before underwriters do.

How do federal minimums affect the need for tailored fleet coverage?

Federal insurance minimums for commercial trucking are set by FMCSA and have not been meaningfully updated in decades. The current thresholds are $750,000 for general freight, $1 million for oil transport, and $5 million for hazardous materials. These numbers were established when medical costs, litigation verdicts, and vehicle replacement values were a fraction of what they are today.

The practical consequence is that FMCSA minimums are inadequate for catastrophic crash coverage given current medical cost inflation and jury verdict trends. A single serious crash involving multiple vehicles, fatalities, or severe injuries can generate liability exposure well above $750,000. Nuclear verdicts, where juries award $10 million or more, have become a documented pattern in commercial trucking litigation. A fleet carrying only the federal minimum is exposed to the gap between that limit and the actual judgment.

Tailored fleet policies address this directly. By setting liability limits based on actual exposure, cargo value, route risk, and operational scale, a customized program provides gap protection that the federal floor does not. This is not optional risk management for large fleets. It is a financial survival question for any fleet operating in high-traffic corridors or carrying high-value or hazardous cargo.

FMCSA cargo category | Federal minimum | Inflation-adjusted need (estimated) |

General freight | $750,000 | $2M+ |

Oil transport | $1,000,000 | $3M+ |

Hazardous materials | $5,000,000 | $10M+ |

Regulatory filings are a second compliance dimension. FMCSA requires carriers to maintain proof of insurance on file to preserve operating authority. A lapse, even a brief administrative one, can trigger a suspension. Tailored fleet policies managed under a single program with centralized compliance tracking reduce the risk of filing gaps compared to managing multiple individual vehicle policies across different carriers. Review the insurance requirements for trucking companies to understand exactly what filings apply to your operation.

Key takeaways

Tailored fleet policies deliver measurable cost savings, accurate risk coverage, and regulatory protection that standard commercial auto policies cannot match for fleets of any meaningful size.

Point | Details |

Consolidation saves money | Single-policy consolidation cuts per-vehicle costs by 10% to 25%, with total savings reaching 40% when combined with other strategies. |

Blanket policies reduce gap risk | Blanket fleet structures cover new vehicles through audit cycles, eliminating uninsured periods during rapid fleet growth. |

Federal minimums are insufficient | FMCSA thresholds have not kept pace with medical costs or litigation verdicts, making tailored limits a financial necessity. |

Deductible strategy drives premiums | Higher deductibles lower baseline premiums significantly, but only work well for fleets with strong cash flow and low claim frequency. |

Annual market shopping pays off | Carrier pricing shifts yearly, and shopping the market annually produces 10% to 30% in additional savings. |

What I’ve learned about fleet policies that most operators find out too late

I have spent years watching fleet operators make the same expensive mistake: they treat insurance as a fixed cost rather than a managed one. They sign at renewal, file the certificate, and move on. The policy sits untouched until a claim forces a conversation nobody wanted to have.

The operators who get this right think about their fleet policy the way they think about fuel contracts or maintenance schedules. They review it before operational changes, not after. They bring loss run data to renewal meetings. They ask their broker which carriers are actively competing for their fleet class this year, not which carrier they used last year.

The blanket policy structure is one of the most underused tools in fleet risk management. I have seen mid-size fleets carrying scheduled policies with 30 or 40 vehicles, updating endorsements every time a truck is traded. That administrative drag is real, and the coverage gap risk during the update window is also real. Switching to a blanket structure is not complicated, but most operators do not know to ask for it.

The federal minimum issue is the one that concerns me most. The $750,000 general freight floor has been politically static for decades while jury verdicts in trucking cases have climbed sharply. A fleet manager who believes the federal minimum is adequate protection is carrying a risk they cannot see until it materializes. Tailored coverage that sets limits based on actual route exposure and cargo type is the only rational response to that environment.

The personalized fleet strategies that actually work are not exotic. They are disciplined: consolidate, optimize deductibles, use your telematics data, shop annually, and work with a broker who knows fleet underwriting. The fleets that do all five consistently outperform on both cost and claims outcomes.

— Guyorguy

How Insuaria helps fleet operators get coverage right from the start

Getting a tailored fleet policy starts with organizing the right information before a licensed insurance professional ever reviews your account.

Insuaria is a compliance-first intake and referral platform built to simplify exactly that first step. Fleet operators use Insuaria’s structured intake process to organize vehicle details, driver records, cargo types, and operational data so that licensed agency partners can review coverage needs efficiently and accurately. The result is a faster, more organized path to the fleet insurance intake process that gives underwriters what they need to build a policy aligned with your actual risk profile. If you are managing a fleet and want to make sure your coverage review starts with the right information in the right format, Insuaria is built for that.

FAQ

What are tailored fleet policies?

Tailored fleet policies are commercial insurance programs customized to a specific fleet’s vehicle mix, cargo types, driver profiles, and operational risk. They differ from standard commercial auto coverage by using actual fleet data, including loss history and safety scores, to set deductibles, liability limits, and endorsements.

How much can a tailored fleet policy save compared to individual vehicle policies?

Consolidating vehicles under one fleet policy saves 10% to 25% per vehicle, with total savings reaching 15% to 40% when deductible optimization, telematics, and annual carrier shopping are combined, according to First Heritage Insurance Agency.

Why are FMCSA minimum insurance limits not enough for most fleets?

FMCSA minimums, set at $750,000 for general freight, have not been updated to reflect current medical costs or litigation verdicts. A single catastrophic crash can generate liability well above that threshold, leaving fleets financially exposed without tailored higher limits.

What is the difference between a scheduled and a blanket fleet policy?

A scheduled fleet policy lists each vehicle individually and requires an endorsement for every addition or trade. A blanket fleet policy covers all qualifying vehicles through periodic audits, eliminating the uninsured gap risk that scheduled policies create during fleet growth.

How often should fleet managers review their insurance policy?

Fleet managers should review their policy at least annually, ideally 60 to 90 days before renewal. Annual carrier shopping alone can produce 10% to 30% in savings, and operational changes like new cargo types or seasonal drivers require mid-term coverage adjustments to avoid gaps.

Recommended

Comments