How to Manage Trucking Liability: 2026 Fleet Guide

- Guyorguy Laguerre

- 2 days ago

- 11 min read

TL;DR:

Trucking liability involves legal and financial responsibility for injuries, damages, and cargo loss during operations. Managing insurance, compliance, and risk documentation continuously helps fleets avoid coverage lapses and costly claims, while documented safety practices lower premiums. Proper claims handling and thorough recordkeeping are essential for effective liability control and maintaining operating authority.

Trucking liability is defined as the legal and financial responsibility a carrier bears for bodily injury, property damage, and cargo loss caused during commercial operations. Knowing how to manage trucking liability is not optional for fleet operators. The Federal Motor Carrier Safety Administration (FMCSA) mandates minimum liability coverage levels, and failing to meet them can suspend your operating authority within 30 days of a coverage lapse. This guide covers every layer of liability management: insurance requirements, FMCSA compliance, risk reduction tactics, claims handling, and the most common mistakes that cost operators their authority and their margins.

How to manage trucking liability: insurance requirements explained

Trucking liability insurance is the financial foundation of every legal motor carrier operation. The FMCSA sets minimum primary auto liability limits based on freight type. General freight carriers must carry at least $750,000 in coverage. Carriers hauling oil, hazardous materials, or explosives must carry $1 million to $5 million depending on the commodity. These are floors, not recommendations. Most shippers and brokers require higher limits before they will tender a load.

Beyond primary auto liability, two mandatory filings govern your proof of coverage with the FMCSA. The MCS-90 endorsement is attached to your policy and guarantees payment to the public even if a claim falls outside normal policy terms. The BMC-91 or BMC-91X filing is submitted directly by your insurer to the FMCSA as electronic proof that your coverage is active. Both must remain current without interruption.

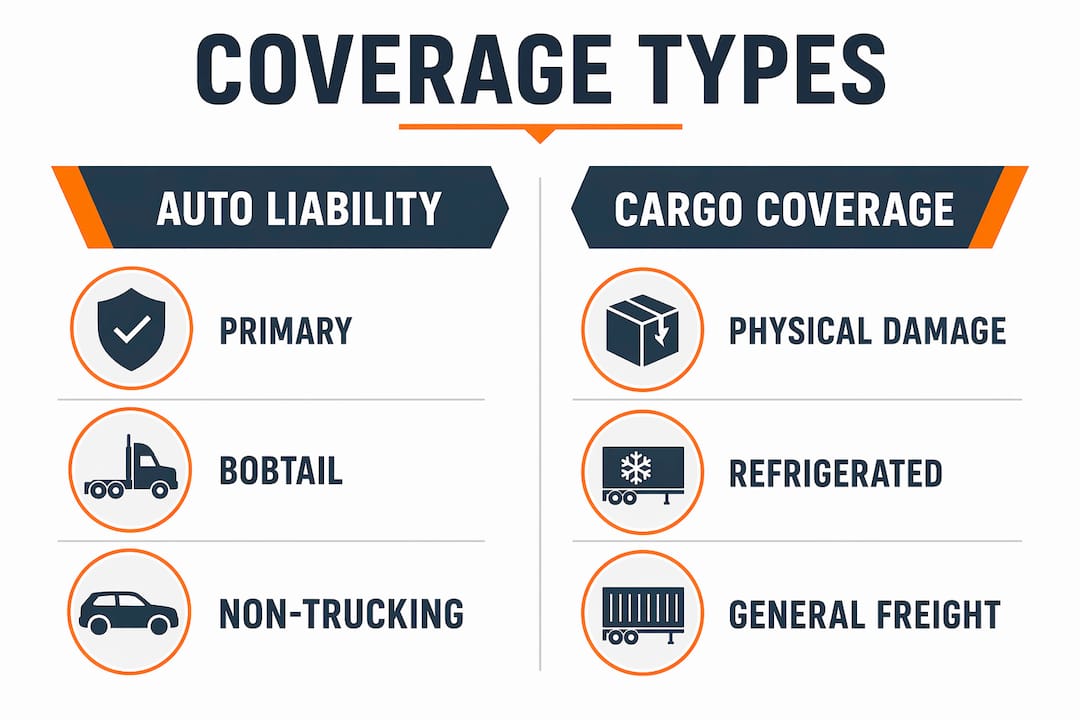

Several additional liability coverage types protect gaps that primary auto liability does not cover.

General liability covers non-driving incidents such as injuries at a customer’s loading dock or property damage during cargo handling.

Bobtail liability covers your tractor when it operates without a trailer and outside of a dispatch, such as driving home after a delivery.

Non-trucking liability covers personal use of the truck when you are not under a motor carrier’s dispatch.

Non-owned trailer liability covers damage to trailers you pull but do not own.

Logistics advisors warn that carrier liability limits often differ from cargo insurance limits, creating gaps that require careful contract review before every load. Cargo liability payouts depend on the lowest cap in a sequence of legal limits, policy sublimits, and deductibles. Matching those layers to your highest-risk freight is the difference between a covered claim and an out-of-pocket loss.

Coverage type | What it protects | FMCSA filing required |

Primary auto liability | Third-party bodily injury and property damage while under dispatch | Yes (MCS-90, BMC-91/91X) |

General liability | Non-driving incidents, loading/unloading injuries | No |

Bobtail liability | Tractor operation without trailer, off dispatch | No |

Non-trucking liability | Personal use of truck, not under dispatch | No |

Cargo liability | Loss or damage to freight in your care | No (but often contractually required) |

Pro Tip: Insurers require a down payment of 10% to 30% of the annual premium to activate coverage. Budget for this upfront cost when planning your operating capital, especially if you are a new entrant.

How to maintain compliance and keep proof of coverage audit-ready

FMCSA compliance is not a one-time task. It is a continuous operating requirement, and the documentation you maintain is as important as the coverage itself. New motor carriers must complete a New Entrant Safety Audit within 18 months of registration, and auditors can request documentation within 48 hours of notice. That window is too short to scramble for records you should already have organized.

The six core areas auditors examine are driver qualification files, hours of service records, drug and alcohol testing programs, vehicle maintenance records, hazardous materials compliance, and financial responsibility documentation. Financial responsibility is where liability management intersects directly with compliance. Your insurance certificates, FMCSA filings, Unified Carrier Registration (UCR), and BOC-3 Process Agent designation must all be current and retrievable on demand.

A coverage lapse is one of the fastest ways to lose your operating authority. When a policy cancels or lapses, your insurer notifies the FMCSA, which can suspend operating authority within 30 days. Reinstatement requires new filings, fees, and sometimes a waiting period. The financial and reputational damage from even a brief suspension far exceeds the cost of maintaining continuous coverage.

Here is a practical compliance workflow to keep your documentation audit-ready at all times:

Maintain a master compliance calendar. Log every renewal date for your insurance policy, UCR registration, BOC-3 filing, and driver medical certificates. Set alerts 30 to 90 days before each deadline.

Store all documents in a centralized digital system. Physical binders fail audits when pages go missing. Platforms like FileFlo or similar compliance software create searchable, timestamped records.

Conduct monthly driver file reviews. Confirm that each driver’s commercial driver’s license (CDL), medical examiner’s certificate, and drug testing records are current.

Run daily Driver Vehicle Inspection Reports (DVIRs). Auditors look for consistent daily records, not just a stack of forms produced at audit time.

Verify FMCSA portal filings quarterly. Log into the FMCSA’s Licensing and Insurance portal to confirm your MCS-90 and BMC-91 filings show as active.

Document every maintenance event. Timestamped repair orders and inspection records demonstrate a functioning maintenance program, not just paperwork.

Successful FMCSA audits require demonstrating a continuous compliance rhythm with no gaps over months. Simple possession of documents is insufficient without consistent daily records and timely alerts.

Pro Tip: Review your insurance requirements annually against your actual operations. If you added a new freight type, expanded your fleet, or hired owner-operators, your coverage obligations may have changed without your insurer knowing.

What risk reduction tactics actually lower your insurance premiums

Insurance is only part of liability management. The risk signals you send to underwriters determine whether your premium is competitive or punishing. A 3-year clean safety record combined with dash cams, telematics, and clean DOT inspections is the single most effective factor for lowering premiums according to risk experts. Underwriters price risk, and every piece of documented safety behavior reduces the risk they are pricing.

Telematics systems from providers like Samsara, Motive, or Verizon Connect give underwriters hard data on speeding events, hard braking, and hours of service compliance. Dash cams from providers like Lytx or SmartWitness create exculpatory evidence when your driver is not at fault. Both technologies reduce claim frequency and severity, which directly affects your loss ratio, the number underwriters watch most closely when setting your renewal rate.

Beyond technology, documented driver training programs signal to insurers that you manage human risk deliberately. Defensive driving courses through the Smith System or the National Safety Council, combined with written policies on distracted driving and fatigue management, create a paper trail that supports favorable underwriting decisions. Carriers with documented training programs consistently receive better pricing than those with identical safety records but no training documentation.

Here are the most effective premium reduction strategies supported by industry risk experts:

Install forward-facing and driver-facing dash cams and share footage proactively with your insurer after incidents.

Use telematics to monitor and correct unsafe driving behaviors before they become claims.

Maintain a clean Compliance, Safety, Accountability (CSA) score by addressing violations immediately after each roadside inspection.

Enroll drivers in annual defensive driving refreshers and document completion in their qualification files.

Choose higher deductibles on physical damage coverage if your cash reserves support it, which lowers your annual premium.

Bundle primary auto liability, general liability, and cargo coverage with one carrier when possible to access multi-line discounts.

Shop for coverage 30 to 60 days before renewal with organized loss runs and safety documentation to give underwriters adequate review time for competitive pricing.

Pro Tip: Pull your CSA scores from the FMCSA’s Safety Measurement System (SMS) portal every 30 days. Scores update monthly, and catching a new violation early gives you time to contest it or correct the behavior before your next renewal conversation.

How to manage trucking liability claims and recordkeeping

Claims management is where liability exposure either gets controlled or compounds. The difference between a $15,000 settled claim and a $150,000 litigated one often comes down to how quickly and thoroughly you responded in the first 72 hours. Proactive claims management with dedicated specialists and digital platforms facilitates faster liability assessments and better subrogation recovery outcomes.

Assign a specific person inside your organization to own every claim from first notice of loss through final resolution. That person should collect the police report, driver statement, photos, dash cam footage, electronic logging device (ELD) data, and any witness contact information within 24 hours of an incident. Delayed evidence collection is the single most common reason claims escalate into litigation.

Third-party claims administrators (TPAs) like Veritas Claims or similar specialists offer objective liability assessment, legal coordination, and subrogation recovery services that most small fleets cannot replicate internally. For fleets running fewer than 20 trucks, the cost of a TPA is almost always lower than the cost of mismanaged claims. For larger fleets, a hybrid model works well: internal staff handles first notice of loss and documentation, while the TPA manages legal exposure and recovery.

Claims approach | Advantages | Disadvantages |

In-house administration | Direct control, lower per-claim cost at scale, faster internal communication | Requires trained staff, risk of bias, limited legal expertise |

Third-party administrator (TPA) | Objective assessment, legal expertise, subrogation recovery capability | Per-claim fees, less direct control, onboarding time required |

Hybrid model | Balances cost and expertise, scalable for growing fleets | Requires clear role definition to avoid gaps in ownership |

Subrogation is the process of recovering costs from a liable third party after your insurer pays a claim. Many carriers leave subrogation money on the table because they do not document incidents thoroughly enough to support recovery. Using a digital claims platform to upload and organize incident records from the moment of loss gives your insurer and legal team the evidence they need to pursue recovery aggressively.

Common mistakes that create costly trucking liability gaps

The most expensive trucking liability mistakes are also the most preventable. They share a common cause: treating compliance and insurance as administrative tasks rather than operational priorities.

Letting insurance lapse is the most damaging single error. Carriers sometimes allow policies to cancel due to missed payments during slow freight periods, assuming they can reinstate quickly. The FMCSA’s 30-day suspension clock starts the moment your insurer files a cancellation notice. Reinstatement is not automatic and often requires new underwriting, which can result in higher premiums or coverage denials.

Misclassifying operations is the second most common gap. Owner-operators who lease to a motor carrier are covered under that carrier’s policy while under dispatch. But the definition of “under dispatch” is narrower than most drivers assume. Driving to a fuel stop after delivering a load may or may not qualify, depending on your lease agreement. Without bobtail or non-trucking liability coverage, that gap is uninsured exposure.

Other frequent mistakes include:

Carrying the FMCSA minimum liability limit of $750,000 when your broker contracts require $1 million or more, which disqualifies you from loads without a mid-term endorsement.

Failing to update your insurer when you add drivers, change freight types, or expand into new states, which can void coverage on unreported operations.

Missing UCR renewal deadlines, which expire annually on December 31 and must be renewed before January 1 to maintain legal operating status.

Submitting BOC-3 filings with outdated process agent information, which creates service of process failures in litigation.

Neglecting to verify that your cargo liability limits match the actual value of freight you haul, leaving you exposed on high-value shipments.

Pro Tip: Schedule a quarterly 30-minute review with your insurance agent specifically to discuss operational changes. Agents who specialize in trucking, such as those working with programs from Canal Insurance, Great West Casualty, or Progressive Commercial, will flag coverage gaps you may not recognize on your own.

Key takeaways

Effective trucking liability management requires continuous compliance, adequate insurance coverage, and proactive risk documentation working together as a single system.

Point | Details |

Know your FMCSA minimums | Primary auto liability starts at $750,000 for general freight and reaches $5 million for hazmat operations. |

Never let coverage lapse | A single lapse triggers an FMCSA notification and can suspend your operating authority within 30 days. |

Build a compliance rhythm | Daily DVIRs, monthly driver file reviews, and 30 to 90-day renewal alerts prevent audit failures. |

Reduce risk to reduce premiums | Dash cams, telematics, clean CSA scores, and documented training programs are the strongest underwriting signals. |

Manage claims proactively | Assign ownership, collect evidence within 24 hours, and use digital platforms to support subrogation recovery. |

What 15 years of watching fleets get this wrong taught me

Most fleet operators I have worked with understand that they need insurance. Far fewer understand that insurance is the last line of defense, not the first. The carriers who manage liability best are the ones who treat their safety program, their driver files, and their compliance calendar as revenue-generating assets. Because that is exactly what they are. A clean loss ratio and a strong CSA score translate directly into lower premiums, better broker relationships, and access to higher-paying freight lanes that require proof of superior safety performance.

The documentation quality I see in claims situations is often the deciding factor between a carrier who recovers quickly and one who does not. I have watched carriers with legitimate defenses lose cases because their dash cam footage was overwritten, their driver statement was taken three days late, or their maintenance records had a six-week gap that opposing counsel used to argue negligence. Evidence discipline is not bureaucracy. It is the difference between a manageable claim and a business-ending judgment.

One observation that surprises most operators: underwriters are not just pricing your past losses. They are pricing your future behavior. When you submit an organized renewal package with 36 months of clean inspections, documented training completions, and a written safety policy, you are telling an underwriter a story about how you will behave next year. That story is worth real money in premium savings. Carriers who invest in compliance infrastructure consistently pay less for the same coverage than those who treat insurance as a commodity purchase.

The uncomfortable truth about cost control in trucking liability is that the cheapest path is also the most disciplined one. Cutting corners on coverage limits or skipping driver training to save money in the short term creates the exact conditions that generate large claims and premium spikes. The operators who spend the most time on compliance spend the least on claims.

— Guyorguy

Get your trucking insurance intake organized with Insuaria

Managing trucking liability starts with having the right coverage in place, and that starts with organizing the information licensed insurance professionals need to review your situation accurately.

Insuaria is a compliance-first insurance intake platform built for trucking businesses. Through simple intake forms, Insuaria helps you organize the details related to your fleet, operations, and coverage needs before a licensed agency partner follows up to discuss your options. Whether you are a single owner-operator or managing a growing fleet, you can start your trucking intake online in minutes. For fleet operators with broader business coverage needs, the business insurance intake covers the full scope of your operation. Insuaria does not bind coverage or issue quotes. All coverage decisions are handled by licensed insurance professionals.

FAQ

What are the FMCSA minimum liability requirements for trucking?

The FMCSA requires a minimum of $750,000 in primary auto liability coverage for general freight carriers. Carriers hauling hazardous materials must carry between $1 million and $5 million depending on the commodity type.

What happens if my trucking insurance lapses?

Your insurer is required to notify the FMCSA when coverage cancels or lapses, and the FMCSA can suspend your operating authority within 30 days. Reinstatement requires new filings and may involve higher premiums or a new underwriting review.

What is the difference between bobtail and non-trucking liability?

Bobtail liability covers your tractor when it operates without a trailer, regardless of dispatch status. Non-trucking liability covers personal use of the truck specifically when you are not under a motor carrier’s dispatch. Owner-operators leased to a carrier typically need both to close coverage gaps.

How do I lower my trucking insurance premiums?

A clean CSA score, dash cam footage, telematics data, and documented driver training programs are the strongest factors underwriters use to price risk favorably. Shopping for coverage 30 to 60 days before renewal with organized submissions also produces more competitive rates.

How should I manage cargo liability differently from auto liability?

Cargo liability payouts depend on the lowest cap across legal limits, policy sublimits, and deductibles. Review your cargo liability coverage against the actual declared value of your highest-risk freight to confirm you are not underinsured on specific load types.

Recommended

Comments